Trade Policy Shifts and Sector Realignments Influence Global Market Trajectory

Medical Equipment Emerges as Fastest Growing Sector While Metals and Minerals Face Sustainability Headwinds

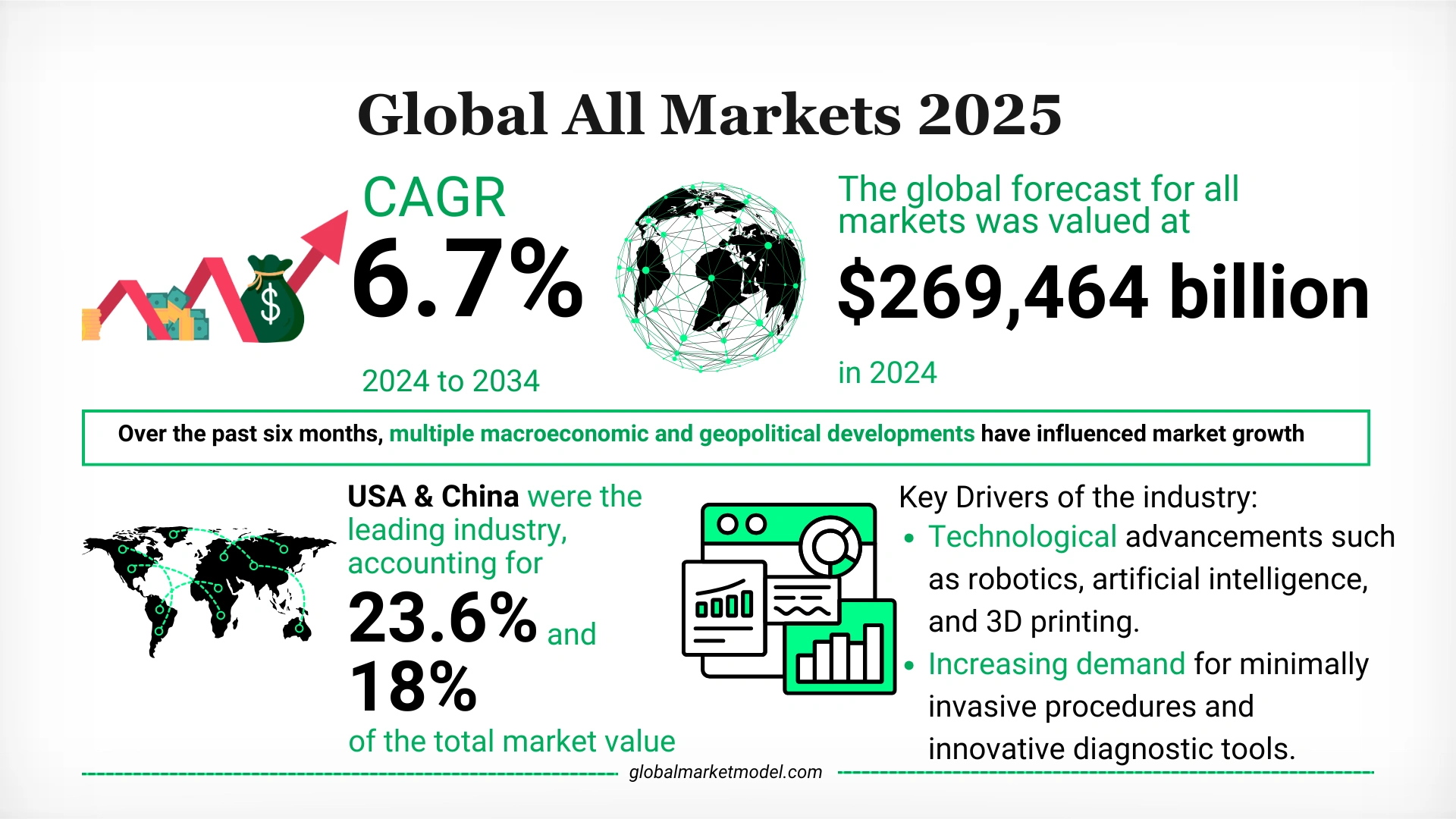

According to the latest forecast from the Global Market Model, the overall market is projected to grow at a compound annual growth rate (CAGR) of 6.7% from 2024 to 2034. Among all sectors, the medical equipment market is expected to see the fastest growth, expanding at a CAGR of 8.9% during the same period. This strong momentum is fueled by technological advancements including robotics, artificial intelligence, and 3D printing, as well as rising demand for minimally invasive treatments and innovative diagnostic solutions.

Conversely, the metal and mineral market is forecasted to be the slowest-growing, with a CAGR of 4.5% between 2024 and 2034. The industry is under pressure from the global shift toward decarbonization, which is dampening demand for traditional metals, particularly those linked to fossil fuel-dependent sectors. Growth is further constrained by rising investment in renewable energy, more efficient recycling systems, and increasing adoption of lightweight materials across manufacturing industries.

In 2024, the total market value across all sectors stood at $269,464 billion. The retail and wholesale, financial services, and services sectors were the top three contributors, comprising 31.6%, 12.5%, and 5.9% of the total market, respectively. The United States and China remained dominant, accounting for 23.6% and 18% of the total market value.

What are the Key Developments Shaping Near-Term Market Dynamics?

In the last six months, several macroeconomic and geopolitical changes have influenced forecast revisions across key sectors:

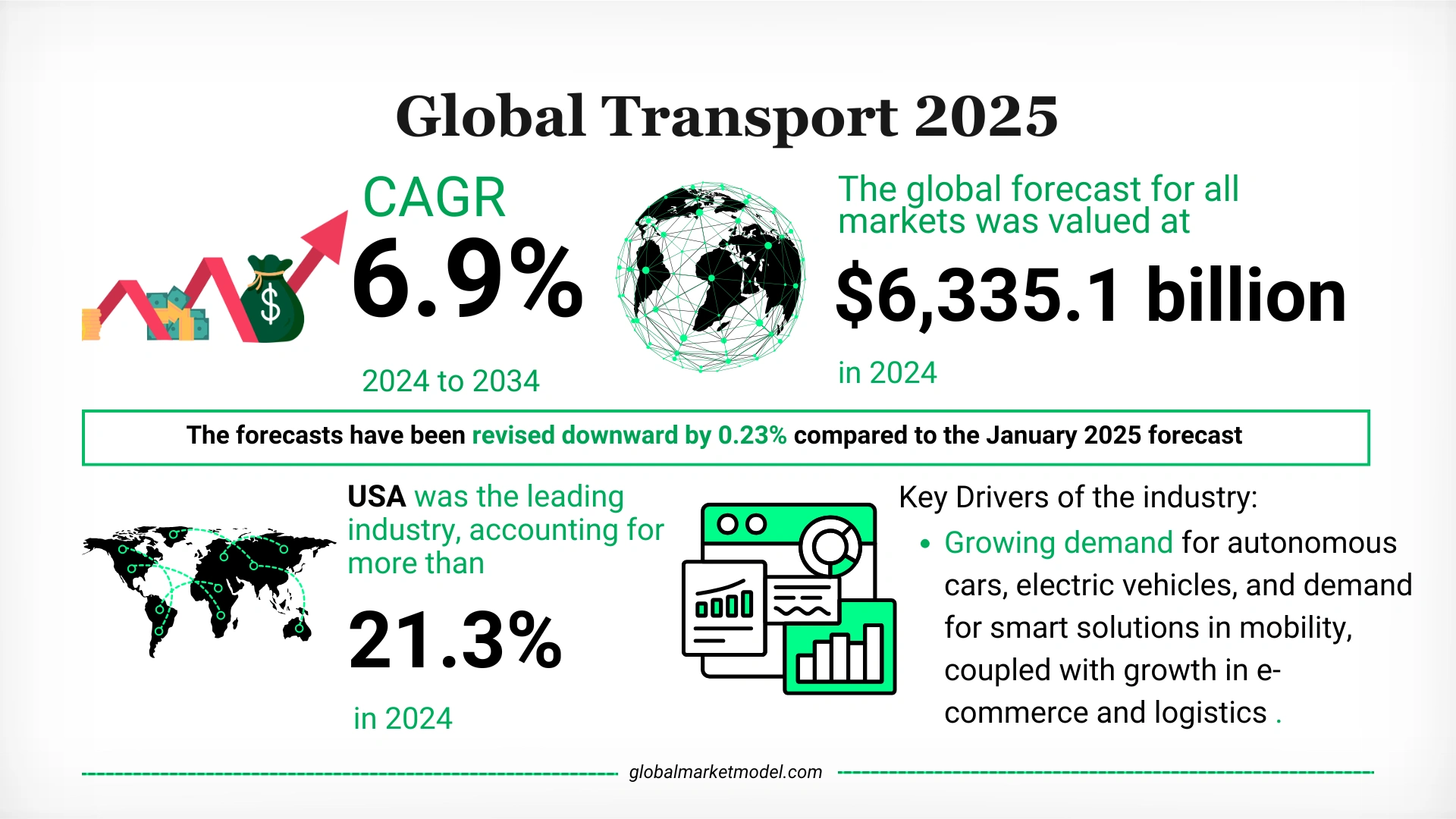

- Transport: Forecasts were lowered by 0.23%, reflecting subdued consumer sentiment, declining trade in auto parts, and tariff-related disruptions to EV and vehicle supply chains.

- Electrical and Electronics: Forecasts declined by 0.27%, largely due to reduced global hardware demand and trade uncertainty tied to newly introduced U.S. tariffs on Chinese semiconductors and battery components.

- Metal and Mineral: Forecasts adjusted down by 0.28% amid weaker construction activity, muted industrial demand in China, and elevated trade risks affecting commodity exports like aluminum, steel, and rare earth metals.

These changes have been primarily influenced by renewed tariff tensions. The announcement of additional U.S. tariffs under the Trump administration has reintroduced uncertainty into global trade, raising concerns about input costs and supply chain disruptions, particularly for sectors reliant on components such as machinery, semiconductors, and consumer electronics.

In response, multinational companies are accelerating supply chain diversification, increasingly shifting operations to regions such as Vietnam, India, and Mexico in an effort to mitigate geopolitical and tariff-related risks.

What are the Emerging Trends and Sector-Level Observations?

- Tariff-Driven Forecast Adjustments: Recent U.S. tariff announcements on Chinese EVs, batteries, and tech components have impacted sectors including transport (-0.23%), electrical and electronics (-0.27%), and metals and minerals (-0.28%).

- Supply Chain Diversification: While large-scale relocation is limited, there is a clear movement toward diversifying procurement strategies and introducing redundancy in high-risk categories.

- AI Infrastructure Expansion: Continued investment in data centers, AI hardware, and model training infrastructure is supporting tech-driven sectors like IT, financial services, and electronics despite macroeconomic pressures.

- Steady Consumer Demand in the West: The U.S. economy remains relatively resilient, with easing inflation, stable interest rates, and strong employment trends driving growth in retail, hospitality, and financial services.

- Mixed Signals from China: While China's industrial and export sectors remain soft, sluggish construction and housing demand continue to weigh on commodity-intensive markets.

- Sustainability Commitments Hold Firm: Investment in green infrastructure, renewables, and sustainable packaging remains on track, supporting steady expansion in utilities, chemicals, and machinery.

- Cautious Capital Spending: Global firms remain cautious on large-scale investments, particularly in commercial construction, IT infrastructure, and premium healthcare equipment, due to rising costs and policy uncertainty in an election year.

The Global Market Model offers the most comprehensive database of market forecasts globally. Covering over 30,000+ markets, the forecasts are updated semi-annually to reflect the latest economic indicators, geopolitical developments, and industry-specific trends. This latest forecast revision was published in July 2025, updating projections originally made in January 2025.

Want to know more about industry outlooks? Let us help you!

Request a Demo

Emerging Technologies and Defence Challenges Driving Market Growth: Aerospace and Defence Industry Overview

Insights from the Global Market Model reveal how innovation, modernization, and shifting global dynamics are redefining the aerospace and defence industry.

The Global Market Model’s latest forecast highlights the accelerating momentum of the aerospace and defence industry, driven by evolving security needs, modernization initiatives, and technological innovation. Here's a detailed overview of the trends shaping this critical sector’s outlook.

What Are the Key Market Projections and Insights on Aerospace and Defence Industry Growth?

Overall Market Growth:

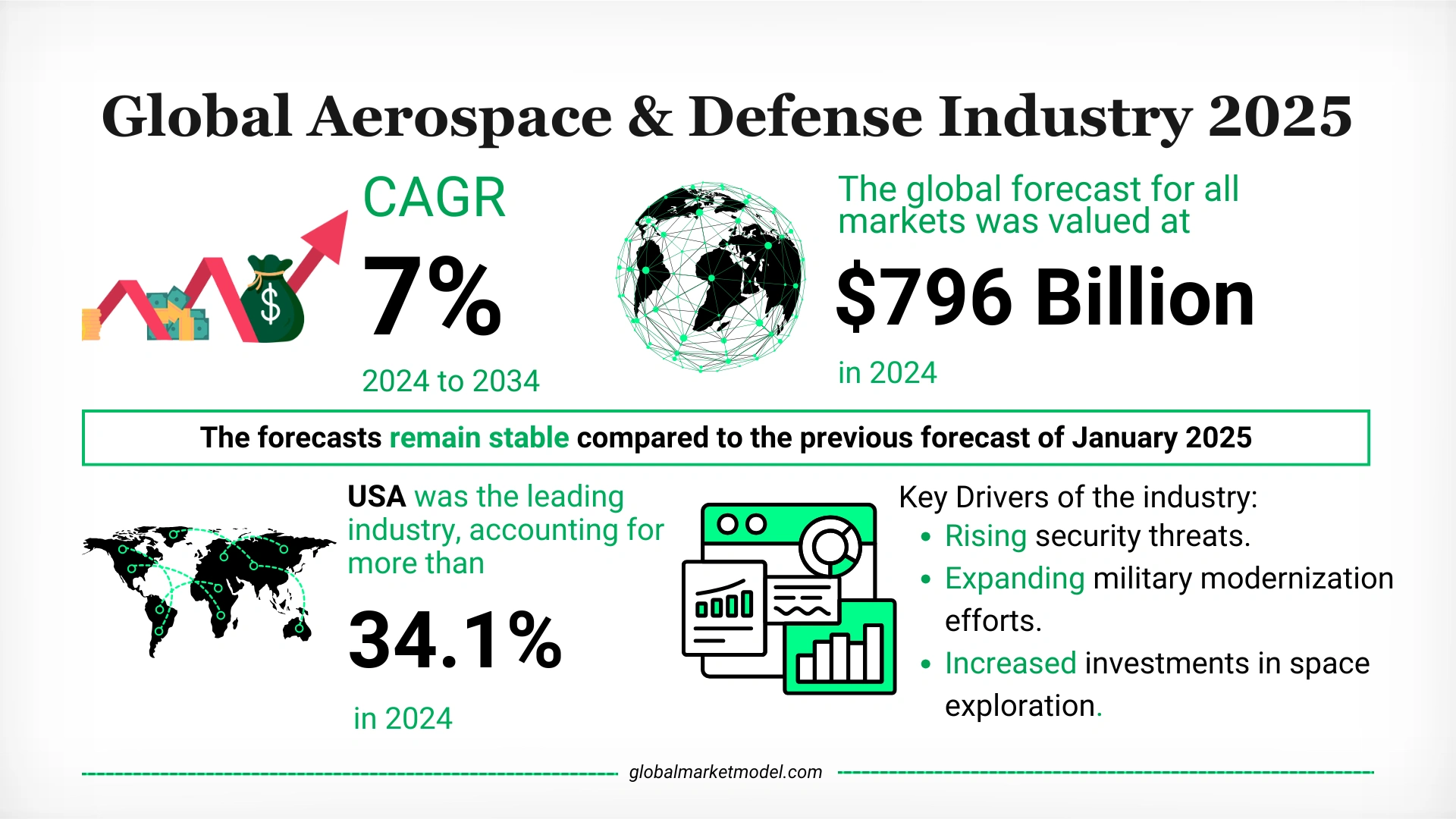

- The global aerospace and defence industry CAGR (compound annual growth rate) is projected to grow at a rate of 7% from 2024 to 2034.

- The aerospace and defence revenue are valued at $796.2 billion in 2024.

- It accounted for 0.6% of the global GDP in 2024.

Growth drivers include:

- Rising global security threats and modernization of military forces.

- Increased investments in space exploration and autonomous systems.

- Advancements in connected defense technologies and surveillance.

- A surge in global air passenger traffic driving commercial aerospace demand.

What Are the key Aerospace and Defence Industry Segments?

Aerospace Segment:

- Focused on the design and manufacture of aircraft, rockets, missiles, and spacecrafts that operate in space.

- Growth is supported by:

- Recovery in the commercial aviation industry.

- Strong government spending on aircraft programs.

- Continuous R&D and new product launches.

- Expanding air passenger traffic worldwide.

Defence Segment:

- Comprises weapons, arms, and military-grade equipment.

- Represents the largest share of the market, accounting for 59.5% of the total in 2024.

- Key growth contributors include:

- High levels of military expenditure.

- Adoption of advanced surveillance and communication systems.

- Innovation in autonomous and connected defence technologies.

- Rising geopolitical tensions and territorial disputes.

What Are the Emerging Trends in the Aerospace and Defence Industry?

Technological Advancements and Modernization:

- Deployment of autonomous systems and drones is increasing.

- Advancements in connected defence ecosystems are streamlining coordination and operations.

- Innovation in space exploration technologies is attracting greater government and private investment.

Civil Aviation Oversight and Quality Control:

- Recent incidents involving Boeing commercial jets have intensified scrutiny of manufacturing and safety protocols.

- Regulatory authorities are increasing focus on quality control and delivery oversight, affecting short-term civil aviation dynamics.

Supply Chain Uncertainty and Global Disruptions:

- Over the past six months, global defence supply chains have experienced increased uncertainty.

- Disruptions in aerospace component movement and defence material procurement have caused production delays.

- This has resulted in a cautious short-term outlook while long-term prospects remain solid.

How Are Geopolitical and Regional Influences Shaping Aerospace and Defence Analysis?

United States

- Maintains its leadership, accounting for 34.1% of the total market in 2024.

- Growth is reinforced by:

- Renewed NATO defence spending commitments.

- Expanded Indo-Pacific naval deployments.

- Significant investments in space-based military programs.

Global Strategic Developments

- Countries such as the U.S., China, and India are boosting defence budgets and space-related defence capabilities.

- Long-term demand for commercial aircraft and modernized defence systems remains strong due to sustained global security concerns and innovation-led investment.

What Is the Overall Outlook for the Aerospace and Defence Industry?

The aerospace and defence market is witnessing steady expansion amid rising geopolitical tensions, technological advancements, and robust government investment. While short-term supply chain disruptions introduce operational challenges, the long-term growth aerospace and defence industry outlook remains resilient, anchored by innovation, security imperatives, and global modernization efforts.

Gain exclusive insights with The Global Market Model, on the key industry metrics of the aerospace and defense industry such as -

- Government expenditure on defense

- Number of enterprises

- Number of employees

Want to know more about the aerospace and defense industry outlook? Let us help you!

Request a Demo

Urbanization, Health Priorities, and Global Demand Driving Agriculture Industry Expansion

Forecasts from the Global Market Model highlight how rising nutritional awareness, sustainable farming, and geopolitical stability are shaping the future of the agriculture industry.

The Global Market Model’s latest forecast emphasizes the strong and steady growth expected in the agriculture market, driven by expanding urban populations, growing demand for healthy food, and increased investment in modern farming techniques. Here’s a comprehensive view of the trends influencing this vital sector.

What Are the Key Market Projections and Insights on Agriculture Industry Growth?

Overall Market Growth:

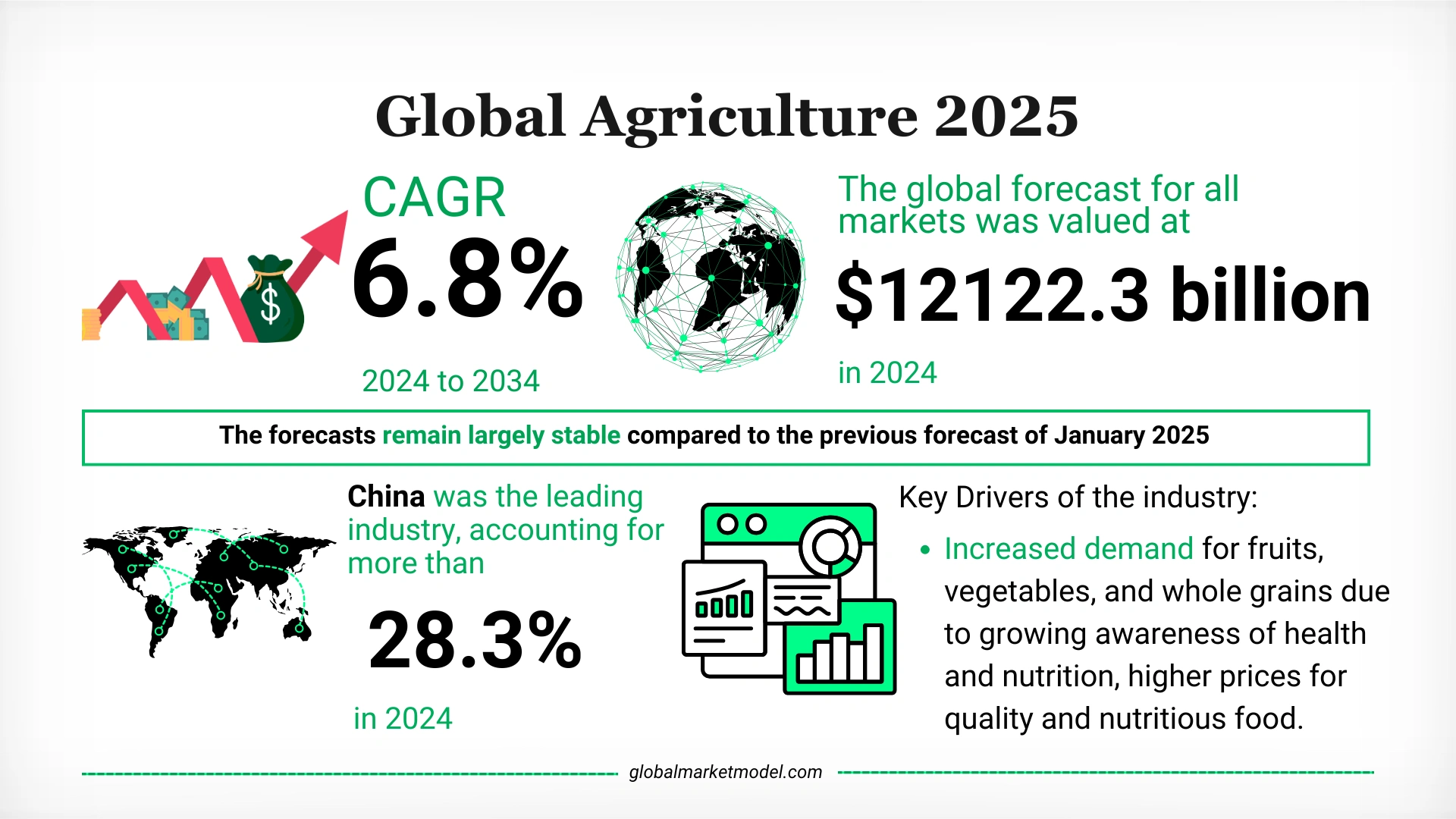

- The global agriculture industry GAGR (compound annual growth rate) is projected to grow at a rate of 6.8% from 2024 to 2034.

- The market is valued at $12,122.3 billion in 2024.

- Agriculture accounted for 10.2% of global GDP in 2024.

- Per capita agriculture industry share stands at $1,417.8 per person per annum.

Agriculture Industry Drivers Include:

- Rising consumer preference for fruits, vegetables, and whole grains.

- Health-conscious dietary shifts increasing demand for nutritious food.

- Higher food prices favouring organic and sustainable products.

- Expanded investment in environmentally responsible farming practices.

What Are the Key Agriculture Industry Analysis?

Crop Production Segment:

- Crop production is the largest segment, accounting for 41.9% of the agriculture market in 2024.

- Growth is driven by:

- Rising demand for staple crops and plant-based foods.

- Expansion of high-efficiency irrigation and seed technologies.

- Supportive policies encouraging sustainable farming.

Animal and Bird Rearing Segment:

- Includes dairy, meat, and poultry production.

- Supported by high global consumption of animal protein.

- Benefiting from increasing disposable incomes and evolving consumer preferences.

- Enhanced by improvements in livestock health management and feed innovation.

What Are the Emerging Trends in the Agriculture Industry?

Sustainable Farming and Organic Practices:

- Surge in demand for organic produce is reshaping farming approaches.

- Governments and private players are investing in low-emission, water-efficient farming systems.

Precision Agriculture and Agri-Tech Adoption:

- Broader adoption of AI, GPS, and drone-based monitoring for higher crop yield and efficiency.

- Data-driven insights are helping optimize resource use and reduce waste.

Stable Global Demand and Supply Chain Resilience:

- International demand for both basic and premium agricultural products remains strong.

- Post-pandemic improvements in logistics and commodity flows support a stable supply outlook.

How Are Geopolitical and Regional Influences Impacting the Agriculture industry Outlook?

China:

- Leading the global agriculture market with a 28.3% share in 2024.

- Boosted by large-scale crop production, high domestic demand, and strategic food security policies.

Global Trade Policies and Tariffs:

- U.S. agricultural tariffs and export regulations continue to impact trade routes and partner dynamics.

- Despite these factors, resilient demand and supply-side investments have helped maintain forecast stability since January 2025.

Regional Development and Food Security Measures:

- Governments worldwide are prioritizing food independence and agricultural self-sufficiency.

- New policies are emerging to protect farmland and incentivize local food systems.

What Is the Overall Outlook for the Agriculture Industry?

The agriculture market is poised for steady growth as health-conscious consumers, technological innovation, and sustainable practices reshape the global food system. Despite trade uncertainties, long-term forecasts remain strong, supported by solid investment in smart farming and stable global demand.

Gain exclusive insights with The Global Market Model on key industry metrics in the agriculture sector, including:

- Arable land

- Livestock population

- Poultry population

- Area cultivated for grains

- Area cultivated for oil seeds

- Area cultivated for vegetables

- Area cultivated for fruits

- Number of enterprises

- Number of employees

Want to explore the agriculture market outlook further? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and sector-specific factors. The current forecast was made in July 2025, revising the previous forecasts made in January 2025.

Industrial Growth and Expanding Applications to Boost Chemicals Industry Expansion

Insights from the Global Market Model show how industrial demand, end-use diversification, and trade shifts are influencing the chemicals industry outlook.

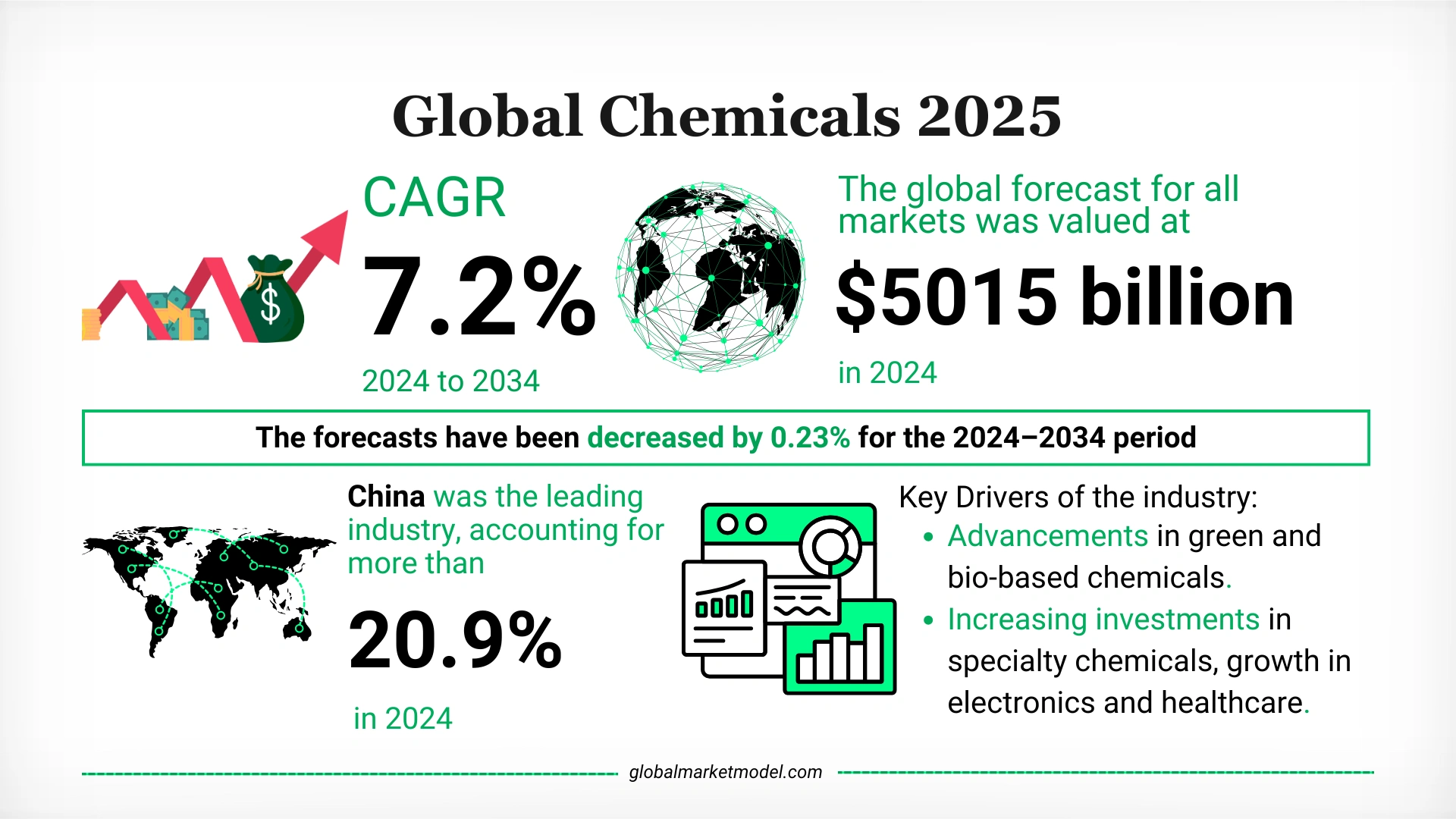

The Global Market Model’s July 2025 forecast sizes the chemicals market at $5,015 billion in 2024, with a projected compound annual growth rate (CAGR) of 7.2% from 2024 to 2034. This outlook reflects strong demand from end-use industries, ongoing urbanization, and a shift toward bio-based and specialty chemicals.

What Are the Key Market Projections and Insights on Chemicals Industry Growth?

Overall Market Growth:

- The chemicals market is valued at $5,015 billion in 2024.

- It represents 4.2% of global GDP in 2024.

- The chemicals industry CAGR is expected to grow at a rate of 7.2% from 2024 to 2034.

Chemicals Industry Growth Drivers Include:

- Advancements in green and bio-based chemicals.

- Rising investments in specialty chemicals.

- Growth in electronics and healthcare sectors.

- Demand from packaging and expanding e-commerce channels.

- Strong support from end-use industries and developed industrial infrastructure.

What Are the Key Segments in the Chemicals Industry?

Market Composition:

- Chemical compounds are produced by transforming organic and inorganic raw materials through chemical processes and product formulation.

- The ethyl alcohol and other basic organic chemical segment was the largest in 2024, accounting for 28.2% of the total market.

What Are the Major Chemicals Industry Trends?

Forecast Revisions and Contributing Factors:

- The July 2025 forecast shows a 0.23% downward revision for the 2024–2034 period compared to January 2025.

- Reasons for the revision include:

- Rising concerns over global trade disruptions linked to proposed U.S. tariffs on chemical exports.

- Ongoing uncertainty around cross-border supply chains.

- Weaker demand from automotive and construction sectors.

- Feedstock price volatility, especially for natural gas and petrochemical derivatives.

- Slower-than-expected growth in demand for sustainable and specialty chemicals.

How Are Geopolitical and Regional Influences Shaping the Chemicals Industry Scope?

Regional Insights:

- China was the leading market in 2024, contributing 20.9% of the global total.

- The market is supported by:

- A large agriculture sector in both developed and developing economies.

- Regulatory focus on pollution control.

- A large consumer population and well-developed industrial base.

What Is the Overall Chemicals Industry Outlook?

Despite a slight downward revision in growth projections, the chemicals industry overview remains strong, supported by industrial demand, technological progress in bio-based solutions, and global urbanization. However, caution persists due to trade-related uncertainties, feedstock cost pressures, and slower recovery in major end-use sectors.

Gain exclusive insights with The Global Market Model on key metrics in the chemicals industry, including:

- Number of enterprises

- Number of employees

Want to know more about the chemicals industry outlook? Let us help you!

Request a Demo

Infrastructure Expansion and Green Construction to Propel Long-Term Construction Industry Growth

Global Market Model insights highlight how sustainability initiatives, smart infrastructure, and regional investment are shaping the construction industry's outlook.

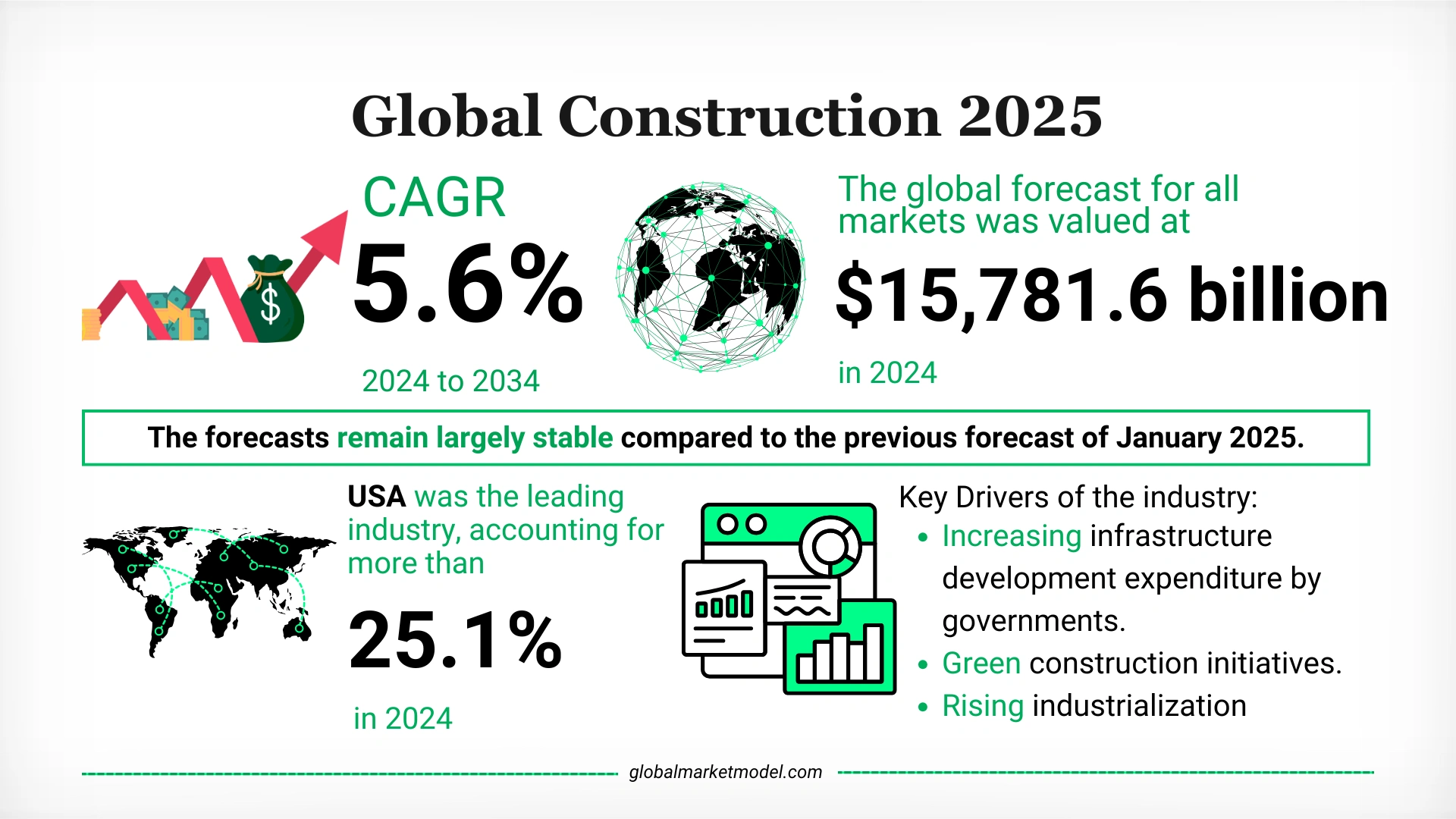

The Global Market Model’s July 2025 forecast values the global construction market at $15,781.6 billion in 2024, with projected growth at a compound annual growth rate (CAGR) of 5.6% from 2024 to 2034. Green building efforts, increased infrastructure spending, and urban development are among the key forces driving growth across regions.

What Are the Key Market Projections and Insights on Construction Industry Size?

Overall Construction Industry Forecast:

- The construction market is valued at $15,781.6 billion in 2024.

- It contributes 13.6% to global GDP, with $1,880.9 per capita annual consumption.

- Expected to grow at a CAGR of 5.6% from 2024 to 2034.

Growth drivers include:

- Government infrastructure development initiatives.

- Expansion of green and energy-efficient buildings.

- Increasing focus on smart city projects.

- Rising industrialization and urban population growth.

- High public and private spending on housing and commercial properties.

What Are the Key Segments in the Construction Industry Overview?

Market Composition:

- Construction encompasses building, modifying, or demolishing structures using planned designs.

- The buildings construction segment was the largest in 2024, accounting for 46.4% of the total market.

Leading Regional Market:

- The USA was the top construction market globally, contributing 25.1% of the total value in 2024.

Supporting Factors:

- Large consumer populations in both developed and emerging economies.

- Development of economic corridors to encourage foreign direct investment (FDI) in infrastructure.

What Are the Key Construction Industry Trends?

Forecast Stability and Short-Term Challenges:

- The July 2025 forecast shows minimal changes compared to January 2025.

- However, the industry continues to face:

- Financial stress in China’s property sector.

- Labor shortages and input cost pressures in Western countries.

- Uneven infrastructure funding across global markets.

Potential Trade Policy Impacts:

- Discussions around new U.S. tariffs on construction-related materials (e.g., steel, aluminum, machinery) are raising concerns about:

- Rising project input costs.

- Greater supply chain uncertainty.

Monetary Environment:

- While interest rates are easing in some regions, their benefits for housing starts and project financing are still emerging.

How Are Geopolitical and Regional Influences Shaping the Construction Industry?

Public Investment and Economic Development:

- Governments are focusing on infrastructure expansion and sustainable city planning to stimulate growth.

- Initiatives aimed at attracting foreign investment are driving infrastructure development in emerging markets.

Smart Infrastructure Focus:

- Urban development, smart infrastructure, and climate-aligned construction practices are increasingly central to long-term strategy.

What Is the Overall Construction Industry Outlook?

The construction industry is positioned for consistent long-term growth, underpinned by sustainability efforts, smart infrastructure spending, and rising demand for housing and urban infrastructure. While short-term concerns around input costs, labor shortages, and property sector volatility persist, the overall market outlook remains stable and forward-looking.

Gain exclusive insights with The Global Market Model on key metrics in the construction industry, including:

- Number of households

- Construction spending

- Number of new households

- Number of enterprises

- Number of employees

Want to know more about the construction industry outlook? Let us help you!

Request a Demo

AI Integration and Electrification to Power Electrical and Electronics Industry Growth

Global Market Model highlights how next-gen technologies, digital infrastructure, and regional policy shifts are shaping the future of the electrical and electronics industry.

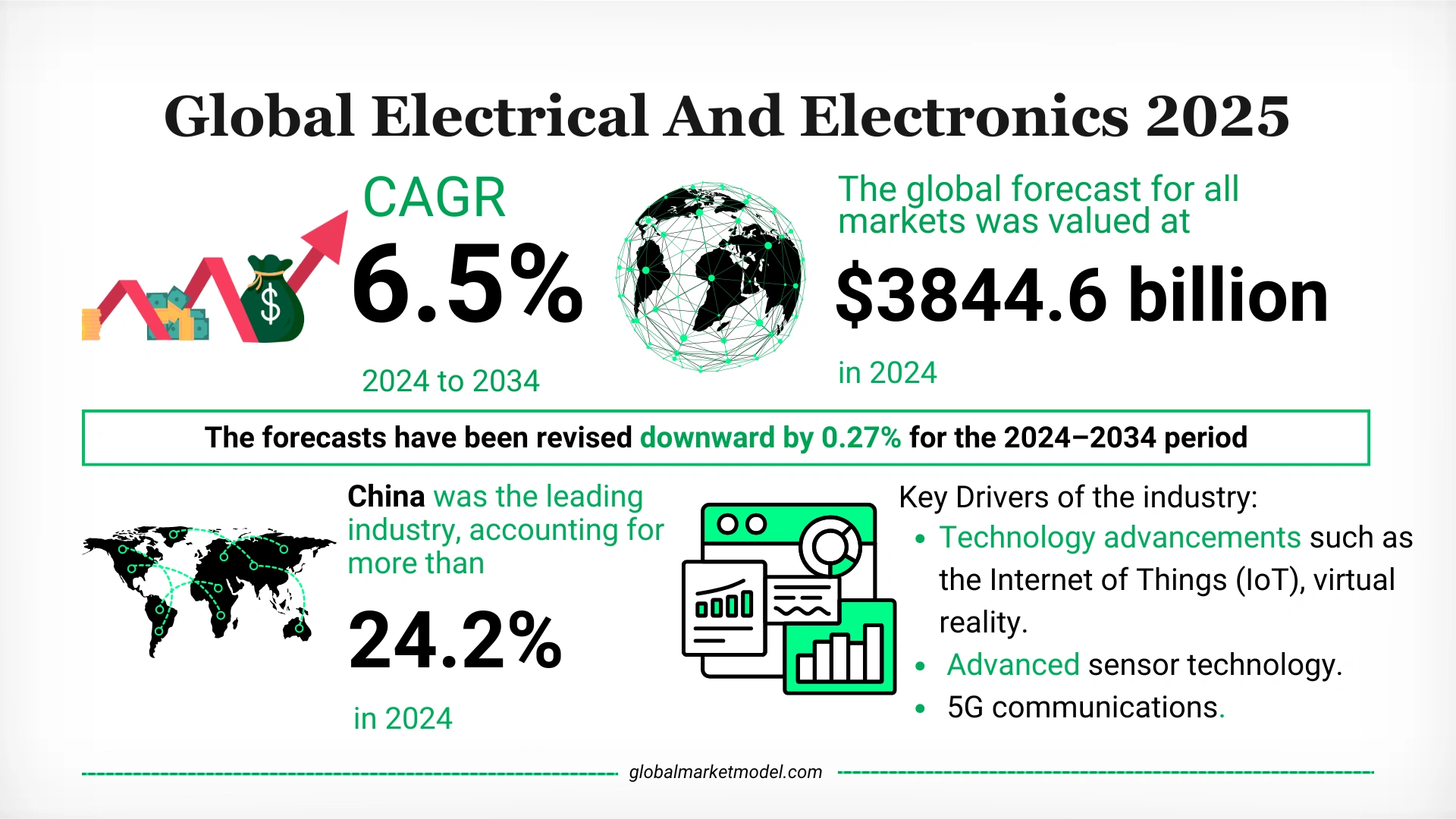

The Global Market Model’s July 2025 forecast values the global electrical and electronics market at $3,844.6 billion in 2024, with a projected compound annual growth rate (CAGR) of 6.5% between 2024 and 2034. Advancements in IoT, AI, and energy-efficient systems are key drivers behind sustained market momentum.

What Are the Key Market Projections and Insights on Electrical and Electronics Industry Size?

Overall Market Growth:

- The electrical and electronics market is valued at $3,844.6 billion in 2024.

- It contributes 3.2% to global GDP, with $448.1 per capita annual consumption.

- Forecasted to grow at a CAGR of 6.5% from 2024 to 2034.

Growth drivers include:

- Increasing adoption of smart home solutions leads to the growth of the electrical and electronics manufacturing market.

- Integration of AI and machine learning into consumer and industrial electronics.

- Advancements in IoT, 5G, virtual reality, and sensor technology.

- Rising investment in renewable energy infrastructure.

- Expansion of electrification in mobility and infrastructure.

What Are the Key Segments in the Electrical and Electronics Industry Analysis?

Market Composition:

- Electrical products include devices that generate, distribute, and utilize electrical power.

- Electronic products contain circuits that may emit physical radiation fields during operation.

- The electrical and electronics market segment was the largest in 2024, accounting for 43.4% of the market.

Leading Regional Market:

- China was the top contributor in 2024, accounting for 24.2% of global revenue.

Supporting Factors:

- A large consumer base in developed and developing nations.

- Growing internet penetration and demand for technological upgrades.

- Increased adoption of electric vehicles.

- Dependence on reliable power systems for critical infrastructure.

What Are the Major Electrical and Electronics Industry Trends?

Forecast Revisions and Influencing Factors:

- The growth forecast has been revised downward by 0.27% for the 2024–2034 period, compared to January 2025.

- Key pressures include:

- Ongoing semiconductor shortages and production delays in Asia.

- Persistent input cost inflation and capacity limitations.

- Proposed U.S. trade tariffs and stricter export controls on technology components, contributing to supply chain uncertainty.

Regional Policy Responses:

- In response to supply concerns, countries such as the U.S., South Korea, and EU have advanced domestic semiconductor production initiatives.

- Programs like the CHIPS Act are backing the construction of new fabs and funding local manufacturing.

How Are Geopolitical and Regional Influences Shaping the Electrical and Electronics industry Overview?

Trade and Supply Chain Factors:

- Discussions around new trade tariffs and export restrictions are creating uncertainty across global supply chains, particularly for intermediate goods and components.

- These shifts impact manufacturers operating in complex global production networks.

Industrial Policy and Investment:

- Governments are increasing support for semiconductor independence to strengthen domestic capacity and reduce supply risks.

- Several new fabrication plant announcements and investment subsidies are in motion.

What Is the Overall Electrical and Electronics Industry Outlook?

Despite near-term headwinds from supply constraints and trade policy uncertainty, the electrical and electronics industry maintains a strong long-term outlook. Sustained demand for AI-enabled technologies, smart devices, and electrification-related components continues to support growth across both consumer and industrial markets.

Gain exclusive insights with The Global Market Model on key metrics in the electrical and electronics industry, including:

- Number of enterprises

- Number of employees

Want to know more about the electrical and electronics industry outlook? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually based on economic, geopolitical, and sector-specific factors. This forecast was published in July 2025, revising the previous version made in January 2025.

From Crypto Scrutiny to Cross-Border Shifts: What’s Powering the Financial Services Industry?

Global Market Model highlights how innovation in financial technology, evolving consumer behaviour, and global investment trends are shaping the future of the financial services industry.

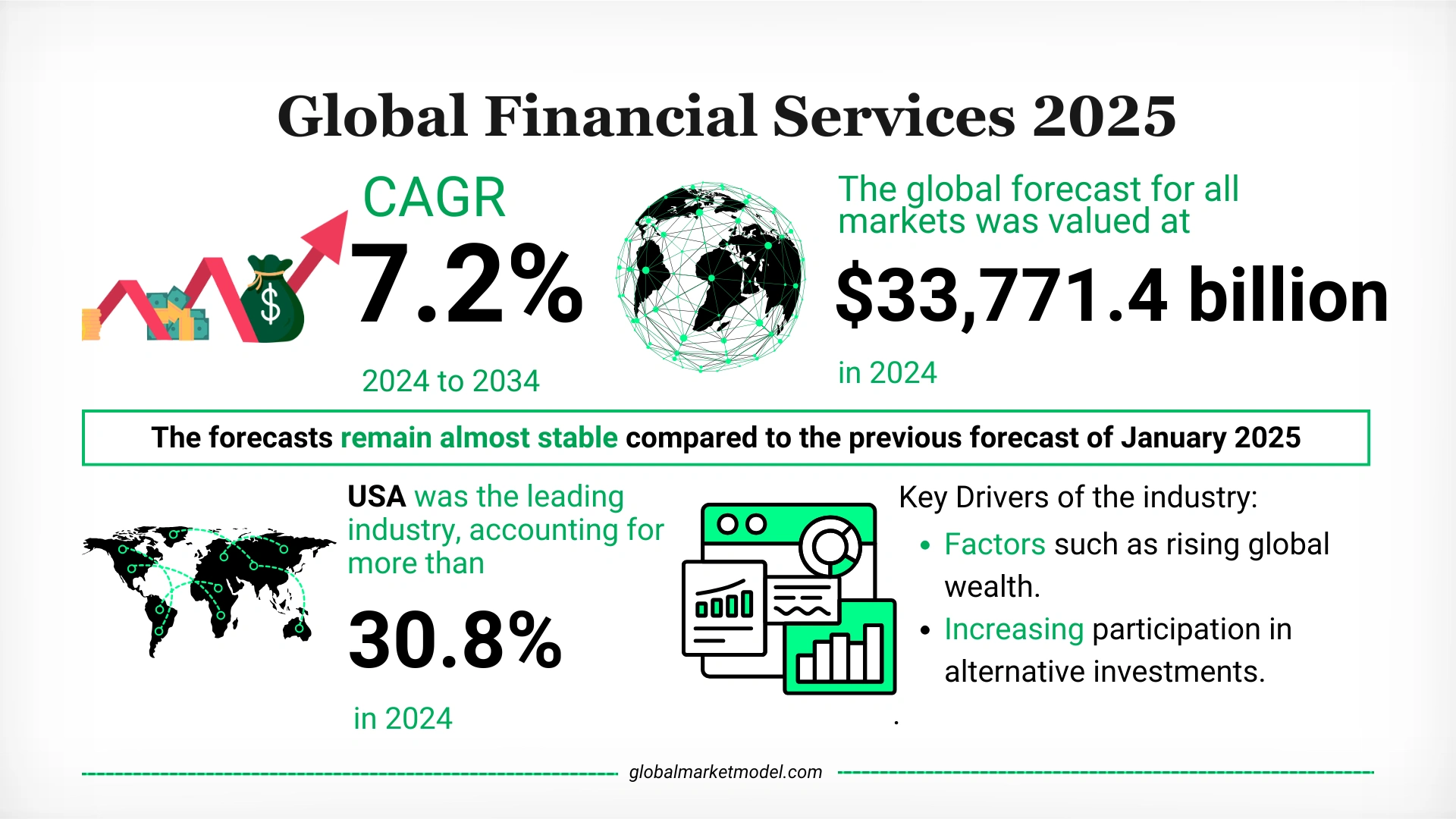

The Global Market Model’s July 2025 forecast values the global financial services market at $33,771.4 billion in 2024, with projected growth at a compound annual growth rate (CAGR) of 7.2% from 2024 to 2034. Expanding access to digital platforms, rising participation in alternative investments, and broader financial inclusion efforts are contributing to the sector’s continued growth.

What Are the Key Market Projections and Insights on the Financial Services Growth Analysis?

Overall Market Growth:

- The financial services market is valued at $33,771.4 billion in 2024.

- It contributes 28.2% to global GDP.

- Expected to grow at a CAGR of 7.2% from 2024 to 2034.

Growth drivers include:

- Rising global wealth and access to diversified investment products.

- Growing participation in alternative investments.

- Blockchain adoption for secure financial transactions.

- Expanding use of AI for financial planning and decision-making.

- Ongoing digital transformation in banking and payments.

What Is the Key Segment in the Financial Services Industry?

Market Composition:

- The industry includes loans, insurance, investment services, credit facilities, and digital money transfers.

- The lending and payments segment was the largest in 2024, accounting for 36.7% of the total market.

Insurance Sector:

- Strongly supported by:

- High healthcare expenditures in developed nations.

- Aging populations in regions such as Europe and Japan.

- Growing middle-class populations in countries like China and India.

Leading Regional Market:

- The USA led globally, accounting for 30.8% of the financial services market in 2024.

What Are the Emerging Trends in the Financial Services Industry?

Forecast Stability and Sector Shifts:

- The latest July 2025 forecast remains largely unchanged from January 2025.

- In the past six months, financial institutions have adjusted to:

- Shifting monetary policies and regulatory frameworks.

- Expectations of interest rate cuts in major economies, driving cautious optimism.

Fintech and Compliance Pressures:

- Increased regulatory scrutiny of fintech, digital lending, and crypto services is reshaping risk management strategies.

- Firms are reassessing compliance procedures to keep pace with evolving standards.

Currency and Cross-Border Transaction Volatility:

- Geopolitical tensions in Eastern Europe and the Middle East have increased foreign exchange market volatility.

- Discussions around U.S. tariffs have added pressure on cross-border financial flows, especially in correspondent banking and FX services.

How Are Geopolitical and Regional Influences Shaping the Financial Services Market?

Digital Infrastructure and Global Connectivity:

- Strong digital infrastructure and real-time payment systems support market growth.

- Continued consumer engagement with both traditional and digital platforms ensures broad market participation.

Policy and Market Reactions:

- Financial institutions are reinforcing currency risk controls.

- Efforts to enhance financial inclusion and modernize payments are gaining momentum globally.

What Is the Overall Financial Services Industry Outlook?

The financial services sector remains resilient, driven by digital innovation, increased financial access, and diversified investment participation. While regulatory shifts and geopolitical volatility present short-term challenges, the long-term outlook remains positive, supported by infrastructure strength and continued technological adoption.

Gain exclusive insights with The Global Market Model on key metrics in the financial services industry, including:

- Number of enterprises

- Number of employees

Want to know more about the financial services industry outlook? Let us help you!

Request a Demo

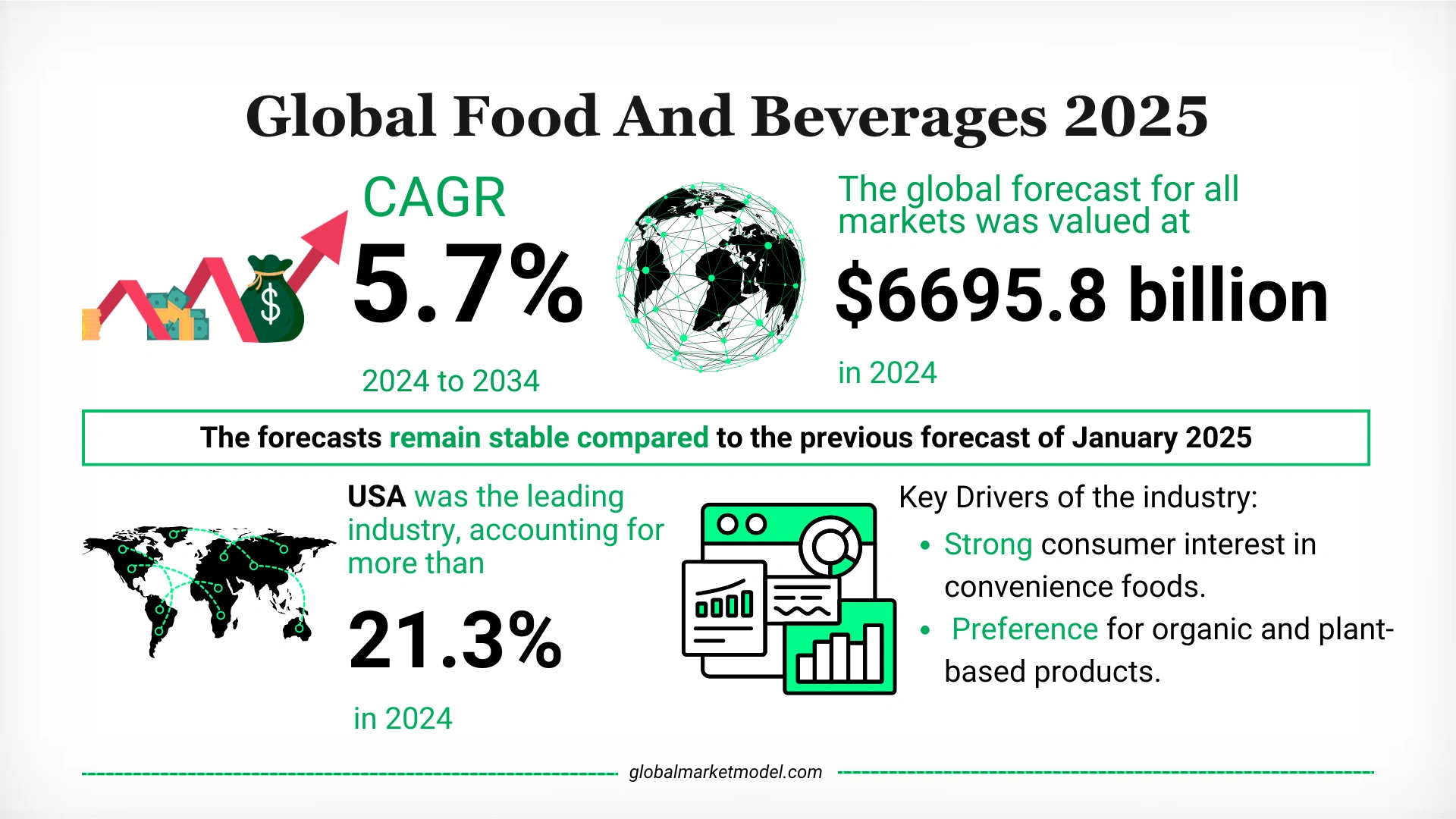

Shifting Lifestyles and Food Innovation Reshaping Market Growth: Food and Beverages Industry Outlook

Insights from the Global Market Model reveal how evolving dietary habits, rising convenience demands, and functional food innovation are redefining the global food and beverages industry.

The Global Market Model’s latest forecast highlights the food and beverages industry growth rate, driven by shifting consumer preferences, increasing demand for plant-based products, and rising interest in time-saving meal solutions. Here's a comprehensive look at the projections and dynamics shaping this essential sector.

What Are the Key Market Projections on Food and Beverages Industry Insights?

Overall Market Growth:

- The global food and beverages market is valued at $6695.8 billion in 2024.

- It is expected to grow at a CAGR of 5.7% from 2024 to 2034.

- The industry accounted for 5.7% of global GDP in 2024.

- Per capita consumption stands at $787.7 per person per annum.

Growth drivers include:

- Rising demand for convenience foods and ready-to-consume options.

- Growing popularity of organic, vegan, and plant-based diets.

- Innovation in individual quick freezing (IQF) and food preservation technologies.

- Increasing fitness and wellness awareness fueling demand for nutritional and functional foods.

What Are the Key Food and Beverages Industry Segments?

Meat, Poultry, and Seafood Segment:

- Largest segment, representing 23.2% of the total market in 2024.

- Strong demand driven by:

- Evolving dietary patterns.

- Government-led nutrition initiatives.

- Expanding fitness-focused consumer base.

Other Key Segments and Consumption Patterns:

- Rapid growth in plant-based alternatives and nutritional beverages.

- Increased consumption of shelf-stable and ready-to-eat products, especially in urban markets.

- USA leads global consumption, accounting for 21.3% of the total market in 2024.

What Are the Emerging Food and Beverages Industry Trends?

Health-Focused Innovation:

- Continued shift towards functional foods addressing specific dietary and health needs.

- Rise in vegan and allergen-free formulations.

Urban Convenience and Shelf-Stability:

- Urban consumers prioritizing shelf-stable, easy-to-prepare meals.

- Growth in time-saving food solutions and nutritional drinks.

Technological Advancements:

- Improved food preservation methods such as IQF.

- Smart packaging and sustainable production processes gaining traction.

How Are Geopolitical and Regional Influences Shaping Food and Beverages Industry Analysis?

United States:

- Holds the largest share globally at 21.3% in 2024.

- Market supported by:

- High disposable income.

- Strong infrastructure for packaged and processed foods.

- Innovations in food delivery and e-grocery models.

Global Developments and Disruptions:

- Proposed U.S. tariffs on food and beverage imports could affect global trade flows.

- Adverse weather patterns in agricultural zones have impacted grain and oilseed supply chains.

- These supply-side pressures have elevated focus on resilient sourcing strategies and domestic food production.

What Is the Overall Food and Beverages Industry Outlook?

The food and beverages industry is poised for consistent growth, underpinned by evolving consumer lifestyles, nutritional awareness, and technological advancements. While regulatory shifts and climate-related disruptions pose challenges, long-term prospects remain strong as manufacturers innovate and adapt to meet global demand.

Gain exclusive insights with The Global Market Model on key industry metrics of the food and beverages industry such as:

- Number of enterprises

- Number of employees

- Livestock primary meat

Want to explore deeper trends in the food and beverages industry? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually based on economic, geopolitical, and sector-specific factors. The current forecast was made in July 2025, revising the previous forecast made in January 2025.

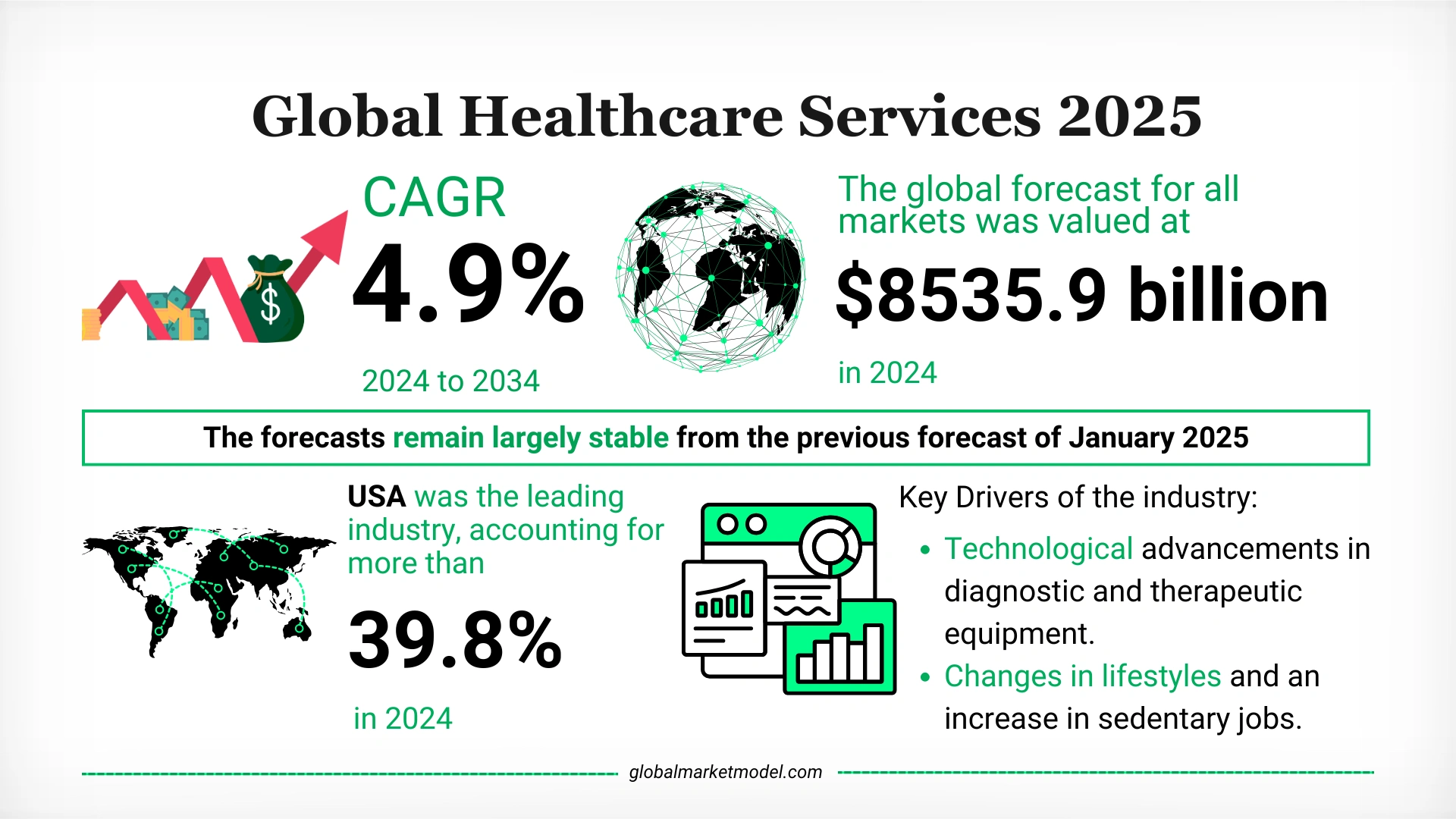

Transforming Access and Advancing Care: Healthcare Services Industry Overview Through 2034

From digital diagnostics to expanding coverage, the Global Market Model highlights how innovation, policy, and population health needs are shaping the future of healthcare services industry.

The Global Market Model’s July 2025 forecast underscores a steadily growing healthcare services market, driven by evolving care delivery systems, home healthcare services, rising disease prevalence, and technological innovation. Here’s an in-depth look at how global healthcare systems are adapting to new challenges and demands.

What Are the Market Projections and Growth of the Healthcare Systems and Services Insights?

Healthcare Services Industry Overview:

- The global healthcare services market is valued at $8535.9 billion in 2024.

- It is expected to grow at a CAGR of 4.9% from 2024 to 2034.

- The sector accounts for 7.3% of global GDP, with per capita spending at $1004 per person annually.

Key Growth Drivers:

- Technological advancements in diagnostic and therapeutic tools.

- Higher prevalence of chronic and age-related diseases such as Alzheimer’s and Parkinson’s.

- Rising demand for medical tourism and better survival outcomes.

- Expanding access to healthcare services in both developed and emerging markets.

Which Segments and Markets Are Leading the Healthcare Services Industry?

By Service Segment:

- Hospitals and outpatient care centres dominate the market, accounting for 53.7% of global healthcare services revenue in 2024.

- These segments benefit from advanced infrastructure, skilled workforce, and growing adoption of integrated care models.

By Region:

- The United States is the leading contributor, representing 39.8% of global healthcare demand in 2024.

- Growth in the U.S. is being fueled by Medicare policy reforms, telehealth expansion, and continued investment in preventive care.

What Are the Emerging Healthcare Services Industry Trends?

Technology-Driven Transformation:

- Countries are ramping up investment in AI-powered diagnostics and clinical decision-making tools.

- Telemedicine and remote monitoring are gaining widespread acceptance, supported by changes in reimbursement structures.

Workforce Challenges and Policy Adjustments:

- Labor shortages and wage inflation have affected service delivery timelines across multiple markets.

- In response, governments are allocating more budget to preventive care and value-based service models.

Global Reforms and Digital Shift:

- The U.S. has enacted Medicare reforms enhancing telehealth coverage and promoting digital-first services.

- Healthcare systems in the UK and Southeast Asia are increasing reliance on digital infrastructure to manage care delivery more efficiently.

How Are Regional and Policy Factors Influencing Central Healthcare Services?

United States:

- Policy-led changes including Medicare updates, expansion of telehealth, and reimbursement reform are shaping care models.

- The focus on value-based care is streamlining services and improving outcomes.

Global Dynamics:

- While labor-related disruptions have temporarily strained some regions, overall demand remains strong.

- Aging populations, chronic disease prevalence, and digital access initiatives continue to support long-term market resilience.

What Is the Global Healthcare Services Outlook?

Despite short-term challenges related to labor costs and service delays, the healthcare services market is set for stable, long-term growth. The continued push toward innovation, improved access, and policy support will enable healthcare systems to adapt to shifting population and care needs, positioning the industry for expanded delivery capacity and improved patient outcomes.

Explore healthcare metrics in detail with The Global Market Model, including:

- Asthma prevalence rate

- Cancer prevalence rate

- Cerebrovascular prevalence rate

- Dermatitis prevalence rate

- Healthcare expenditure

- Hearing loss prevalence rate

- HIV prevalence rate

- Diabetes prevalence rate

- Glaucoma prevalence rate

- Healthcare - number of employees

- Healthcare - number of enterprises

- Hospital beds

- Hypertension prevalence rate

- Number of dentists

Want to dive deeper into the global healthcare services market?

Request a Demo

Forecasts from the Global Market Model are updated semi-annually. The July 2025 forecast reflects revisions made to the January 2025 update, incorporating recent geopolitical, economic, and health system developments.

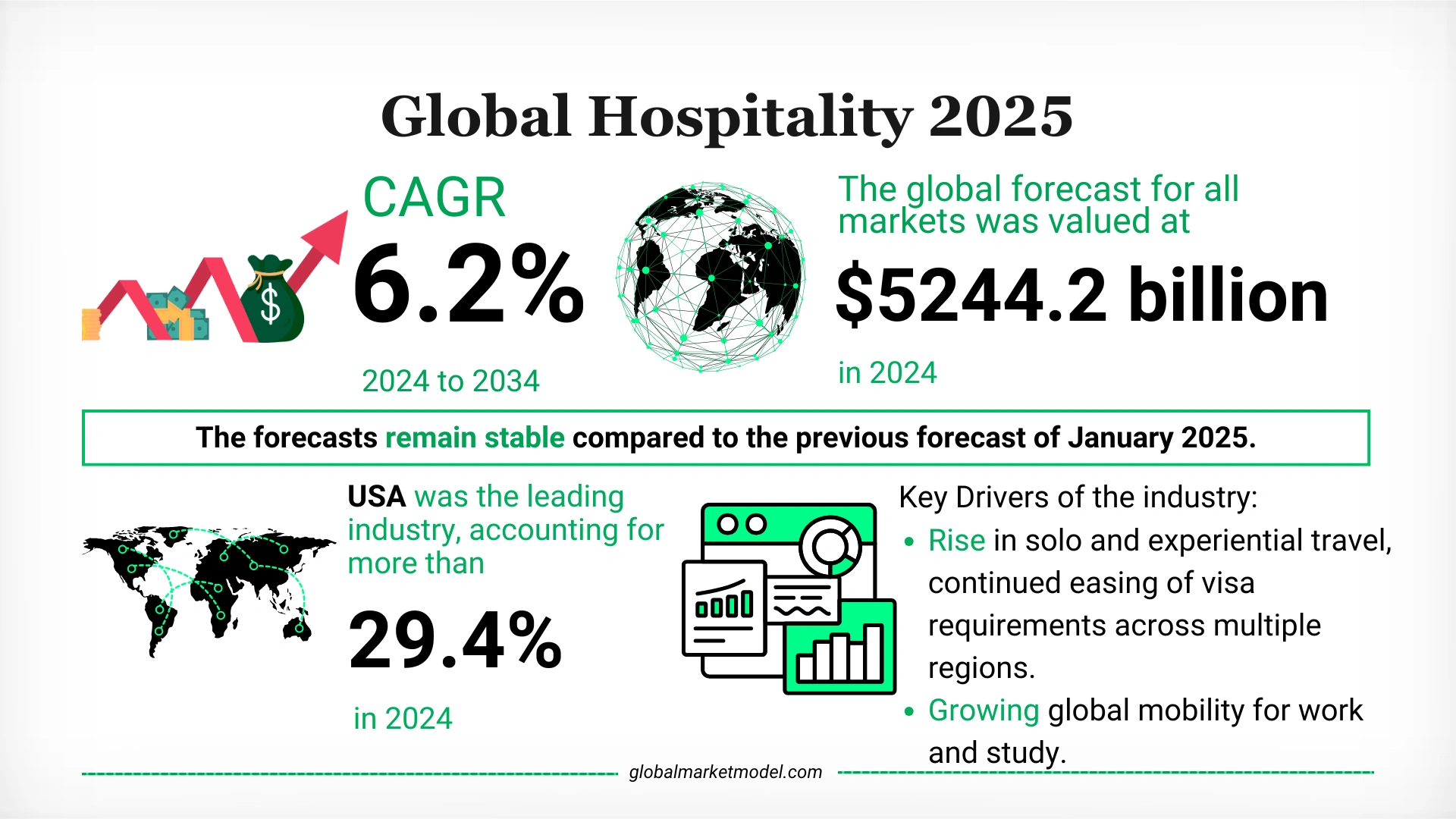

Evolving Travel Patterns and Digitalization Drive the Hospitality Industry

Insights from the Global Market Model reveal how changing travellers behaviours, food consumption trends, and digital innovations are shaping the future of the hospitality industry.

The Global Market Model’s latest forecast highlights how demand for solo and experiential travel, digital booking preferences, and global mobility for work and study are transforming the hospitality industry. Here's a detailed overview of the key dynamics influencing this vital sector.

What Is the Hospitality Industry’s Growth Trajectory?

Overall Market Growth:

- The global hospitality market is projected to grow from $5244.2 billion in 2024 at a CAGR of 6.2% between 2024 and 2034.

- The market accounted for 4.5% of the global GDP in 2024.

- Per capita consumption stood at $617.3 per annum.

Hospitality Industry Growth Drivers:

- Rise in solo and experiential travel.

- Easing of visa requirements in multiple regions.

- Increased mobility for work and study.

- Growing demand for digital booking and personalized services.

- Higher interest in convenience foods and leisure travel experiences.

What Are the Key Segments in the Hospitality Industry?

Food and Beverage Services Segment:

- Accounted for 74% of the total hospitality market in 2024.

- Includes businesses like restaurants and bars offering food and beverage services.

Lodging and Travel Services Segment:

- Includes affordable lodging options such as hostels and capsule hotels.

- Strong demand observed across regions like India, Australia, and New Zealand, particularly for domestic and leisure travel.

Leading Country:

- The United States represented 29.4% of the global hospitality market in 2024.

What Are the Key Hospitality Industry Trends?

AI in Hospitality and Industry:

- Widespread use of digital tools to enhance guest personalization.

- Adoption of AI-driven check-in systems and automated service models.

Return to Events and Social Travel:

- Urban areas are seeing steady footfall in mid-tier lodging and casual dining due to events and social gatherings.

Cost Pressures and Operational Adjustments:

- Rising wages and input prices for food are impacting operations.

- Businesses are balancing cost pressures with steady domestic travel demand.

How Are Geopolitical and Regional Influences Shaping Hospitality Market Trends?

Regional Demand Trends:

- Domestic travel demand remains strong across countries like India, Australia, and New Zealand.

- Gradual recovery of international and business travel observed globally.

Urban Hospitality Industry Overview:

- Urban regions witnessing stable demand in affordable accommodation and food services.

What Is the Overall Outlook for the Hospitality Industry?

The hospitality market is set to grow steadily, supported by resilient consumer interest in food, travel, and social experiences. Despite cost pressures and gradual international travel recovery, digital innovation and stable leisure travel continue to anchor the sector’s positive trajectory.

Gain exclusive insights with The Global Market Model on the key metrics of the hospitality industry such as –

- Inbound international mobile students

- Number of hotel rooms

- Inbound- nights spent in hotels

- Domestic- nights spent in hotels

- Inbound - number of visitors

- Domestic - number of visitors

- Number of tourist arrivals inbound

- Number of enterprises

- Number of employees

Want to explore the future of the hospitality industry? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and sector-specific factors. The current forecast was made in July 2025, revising the previous forecasts made in January 2025.

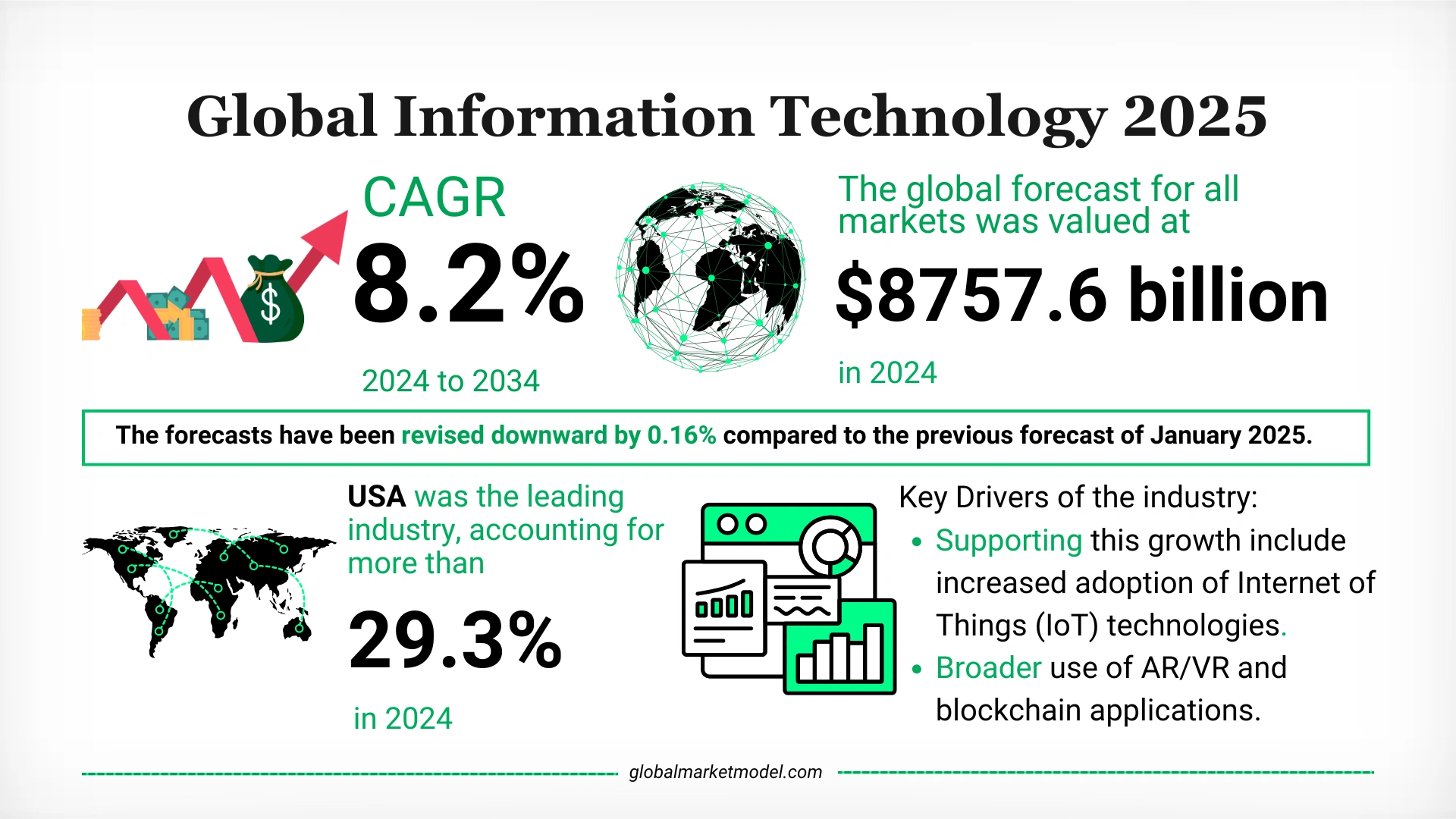

Enterprise Digitalization and AI Investments to Drive Information Technology Industry

Insights from the Global Market Model highlight how digital transformation, connectivity, and innovation are shaping the information technology market’s future.

The Global Market Model’s latest forecast emphasizes the transformative growth trajectory of the information technology industry, underpinned by widespread enterprise digitalization, emerging technologies, and evolving global infrastructure. This overview explores the key metrics influencing the sector’s long-term outlook.

What Are the Key Market Projections and Insights on Information Technology Market?

Informational Technology Industry Growth Rate:

- The global information technology market is expected to grow from $8,757.6 billion in 2024 at a CAGR of 8.2% during 2024–2034.

- The sector accounted for 7.4% of the global GDP in 2024.

Growth drivers include:

- Rising adoption of Internet of Things (IoT) technologies.

- Expansion of e-commerce and smart city initiatives.

- Increased enterprise investments in automation and cybersecurity.

- Rapid development of 5G infrastructure enabling innovation.

- Broader adoption of AR/VR and blockchain applications.

What Are the Key Information Technology Industry Segments?

IT Services Segment:

- Largest segment of the IT market, accounting for 39.1% of the total in 2024.

- Demand is driven by enterprise reliance on managed services, digital platforms, and cloud-based applications.

What Are the Emerging Trends in the Global Information Technology Industry Analysis?

Innovation and Digital Transformation:

- Continued demand for cloud services, artificial intelligence, and enterprise automation.

- Government support for IT infrastructure and policy frameworks enabling tech-driven growth.

Short-Term Challenges and Cost Optimization:

- Enterprises are delaying large-scale IT modernization due to cost-saving efforts.

- AI-related investments remain a focus, but immediate monetization is limited.

Geopolitical and Trade Disruptions:

- Hardware-reliant segments like computer hardware and telecoms are impacted by new tariffs and export restrictions.

- Increased input costs, supplier diversification, and scrutiny of cross-border technology flows are causing slower deployment cycles.

How Are Geopolitical and Regional Influences Shaping the Information Technology Industry?

United States:

- Leading market in the global IT industry, accounting for 29.3% of the total in 2024.

- Market leadership is driven by innovation, enterprise spend, and strong infrastructure support.

Forecast Adjustments and Global Developments:

- Forecasts revised downward by 0.16% from January 2025 to July 2025.

- Adjustments reflect trade uncertainty and macroeconomic shifts affecting hardware and infrastructure-related segments.

What Is the Overall Information Technology Industry Outlook?

Despite short-term headwinds such as cost optimization efforts, trade disruptions, and delayed infrastructure upgrades, the long-term outlook for the information technology market remains strong. Ongoing digital transformation, increasing demand for cybersecurity, and AI-driven innovation continue to support sustained growth across industries.

Gain exclusive insights with The Global Market Model, on the key industry metrics of the information technology market such as –

- Number of internet users

- Number of households with computers

- Number of smartphone users

- Number of households with broadband access

- Number of enterprises

- Number of employees

Want to know more about the information technology market outlook? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and sector-specific factors. The current forecast was made in July 2025, revising the previous forecasts made in January 2025.

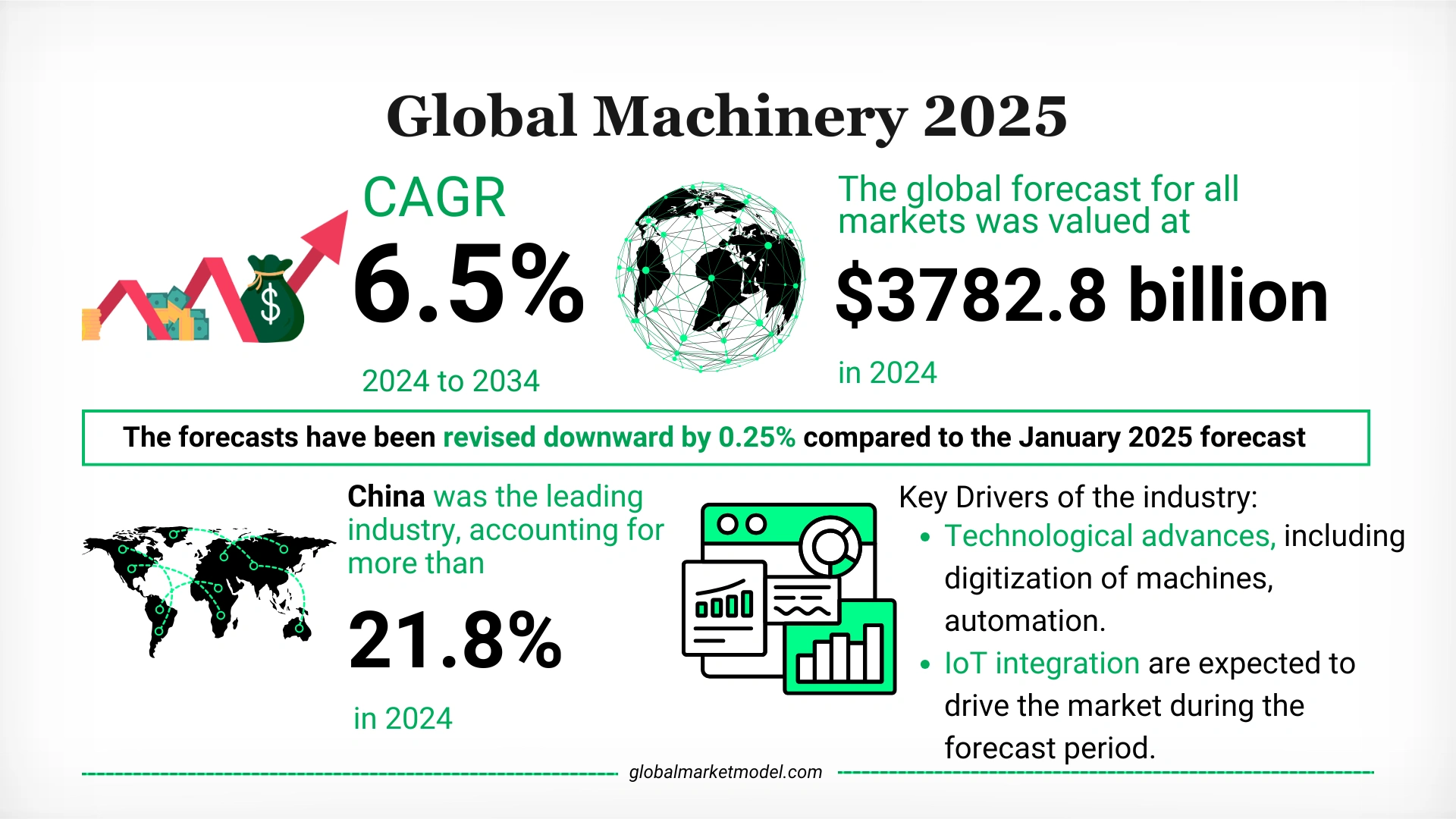

Industrial Automation and Energy-Efficient Solutions Accelerate Market Expansion: Machinery Industry Overview

As per the Global Market Model, the machinery industry is undergoing a major transformation, led by the rise of intelligent systems, green engineering, and growing industrial demand.

The Global Market Model’s latest forecast presents a comprehensive outlook on the machinery industry, showcasing how automation, technological innovation, and shifting capital investment strategies are driving long-term momentum.

What Are the Key Market Projections and Insights on Machinery Manufacturing Industry Growth?

Overall Market Growth:

- The global machinery market is projected to grow at a CAGR of 6.5% from 2024 to 2034.

- Market size is valued at $3,782.8 billion in 2024.

- It accounted for 3.2% of the global GDP in 2024.

Growth drivers include:

- Technological advances such as digitization, automation, and IoT integration.

- Rising investment in smart manufacturing solutions.

- Demand for sustainable and energy-efficient machinery.

- Expanding industrialization across emerging economies.

- Growing use of robotics and advanced material-handling systems.

What Are the Key Machinery Industry Segments?

Agriculture, Construction, and Mining Machinery Segment:

This is the largest segment in the machinery market, representing 20.8% of the total in 2024.

Growth is fueled by:

- Infrastructure development in emerging markets.

- Increasing mechanization in agriculture.

- Mining equipment demand supported by rising commodity extraction.

Other Heavy Machinery Industry Categories:

Include tools and equipment for industrial, energy, and transportation applications.

Growth is supported by:

- High-tech manufacturing adoption.

- Demand for precision machinery and sustainable systems.

- Sector-specific automation across manufacturing and utilities.

What Are the Major Machinery Industry Trends?

Industrial Machinery Industry and Smart Equipment:

- Integration of sensors, AI, and IoT into machinery is driving efficiency and predictive maintenance.

- Adoption of automation and robotics across production environments is increasing.

Energy Transition and Sustainability:

- Shift toward energy-efficient and eco-friendly machinery is gaining traction.

- Equipment built with green materials and lower emissions standards is in demand.

Capital Investment Headwinds and Supply Pressures:

- Input cost volatility and trade policy uncertainty have affected equipment procurement.

- Businesses are delaying purchases or extending replacement cycles due to higher costs and tariffs.

- Small and mid-sized enterprises are particularly affected by import cost escalations and conservative capital planning.

How Are Geopolitical and Regional Influences Shaping Machinery Industry Analysis?

China:

- Leads the global machinery market with a 21.8% share in 2024.

- Growth is driven by strong manufacturing activity, exports, and industrial upgrades.

Global Trends:

- Trade policy changes, especially in the U.S., are impacting import costs for key components like hydraulics, precision tools, and engines.

- Some regions are experiencing selective slowdowns in construction and agriculture-related spending.

- Interest rate easing in major economies is unfolding gradually, influencing business investment sentiment.

What Is the Overall Machinery Industry Outlook?

The machinery market is positioned for steady growth as demand for smart, efficient, and automated systems continues to rise. While recent macroeconomic uncertainties and trade challenges have introduced short-term caution, long-term prospects remain robust due to industrial automation, sustainability mandates, and the modernization of core infrastructure globally.

Gain exclusive insights with The Global Market Model, on key machinery industry metrics such as –

- Number of enterprises

- Number of employees

Want to know more about the machinery industry outlook? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and industry-specific factors. The current forecast was made in July 2025, revising the previous forecast made in January 2025.

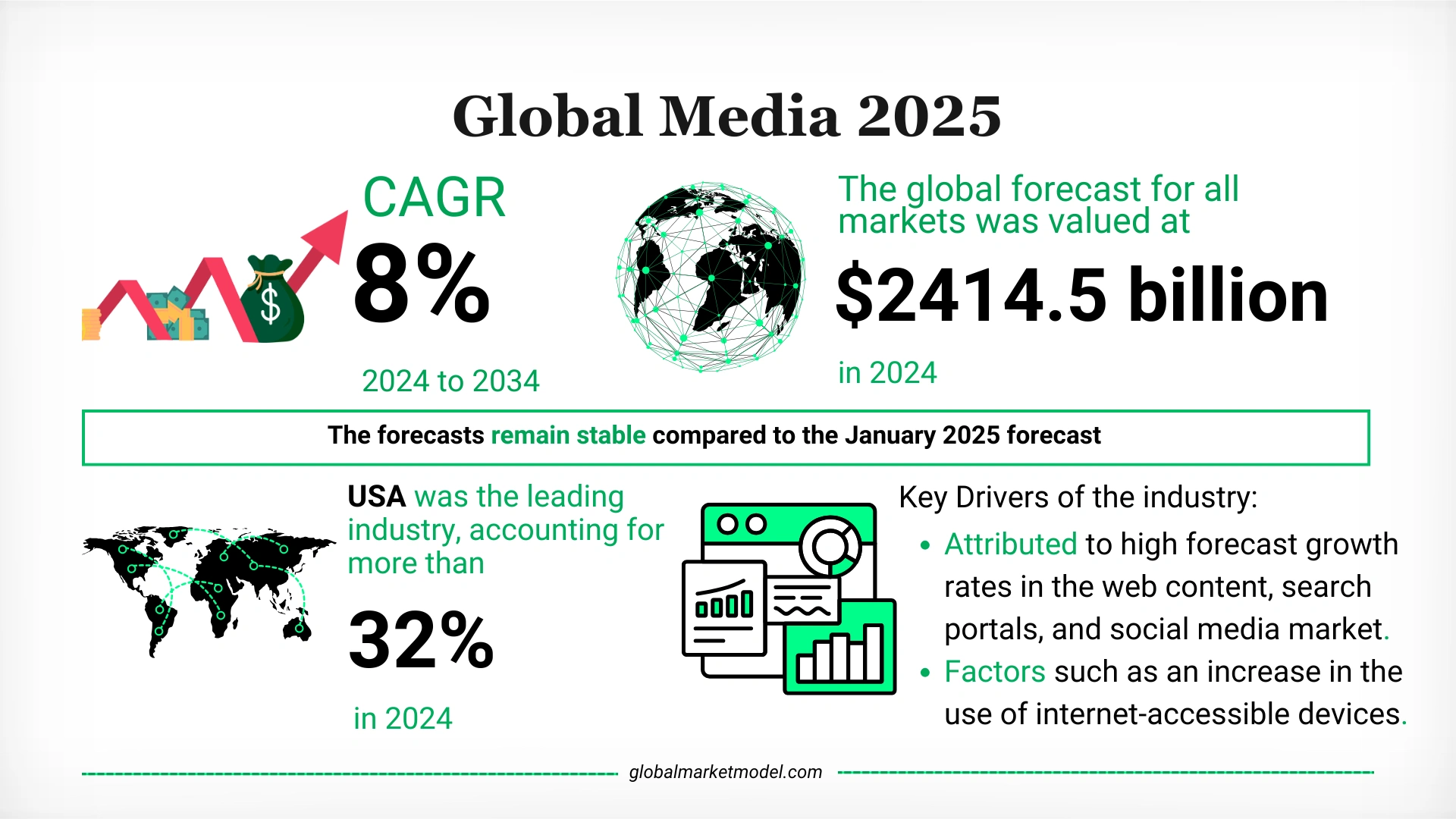

Evolving Channels, Expanding Reach: Media Industry Overview Through 2034

As digital platforms diversify and consumer engagement deepens, the Global Market Model reveals how innovation in content delivery and advertising is reshaping the future of the global media industry.

The Global Market Model’s July 2025 forecast places the global media market at $2414.5 billion in 2024, projecting a compound annual growth rate (CAGR) of 8% from 2024 to 2034. Growth is largely driven by surging demand for digital platforms, interactive content, and immersive media formats. This overview explores how these forces are redefining the media landscape across geographies and channels.

What Are the Market Projections and Growth Insights for the Media Market?

Overall Market Growth:

- The global media market is valued at $2414.5 billion in 2024.

- From 2024 to 2034, the market is expected to grow at a CAGR of 8%.

- In 2024, the media sector represented 2% of global GDP.

Key Growth Drivers:

- Increasing adoption of internet-connected devices and faster network speeds.

- Growing consumer spending on digital content, including films, videos, and streaming services.

- Expanded digital media industry, fueled by web and social media platforms.

- Advancements in augmented reality (AR), virtual reality (VR), and immersive audio-visual technologies.

What Are Leading Types of Media Industry?

By Segment:

- The web content, search portals, and social media industry led the market, comprising 28.3% of total media revenues in 2024.

- This growth reflects strong user engagement, ad-based monetization, and continuous platform innovation.

By Region:

- The United States accounted for 32% of the global media market in 2024.

- Market performance in the U.S. was supported by high entertainment spending and a large base of smartphone and social media users.

What Are the Emerging Trends in the Global Media Market?

Forecast Revisions and Influencing Factors:

Ad-Supported Streaming Models:

- Major platforms like Netflix and Disney+ are rolling out ad-supported subscription tiers across new markets to attract cost-conscious viewers.

Immersive and Interactive Experiences:

- Investments continue in formats such as spatial audio, interactive video, and AR to capture user attention in a saturated content environment.

Digital Advertising Recovery:

- The industry has seen a rebound in digital ad spend, particularly across sectors like travel, FMCG, and retail, supporting broader media growth.

How Are Regional and Economic Factors Influencing the Media And Entertainment Industry?

Stable Forecast Revisions:

- The July 2025 forecast remains consistent with the January 2025 outlook, reflecting ongoing stability in global demand.

- Partial economic caution persists in some consumer segments, but overall engagement with media content remains resilient.

Global Adoption Trends:

- Both developed and developing economies continue to drive demand for diversified media channels, backed by rising internet and mobile penetration.

What Is the Media Industry Outlook?

Despite selective consumer budget constraints, global demand for digital content and advertising remains strong. The media industry is well-positioned for sustained growth, propelled by evolving content formats, diversified monetization strategies, and deepening user engagement across digital ecosystems.

Explore detailed metrics with The Global Market Model, including:

- Number of internet users

- Number of households with computers

- Number of smartphone users

- Number of households with broadband access

- Number of enterprises

- Number of employees

Get more in-depth insights about global media and entertainment industry overview and media industry trends with Global Market Model:

Request a Demo

Forecasts from the Global Market Model are updated semi-annually. The July 2025 forecast reflects updates from January 2025, accounting for economic, policy, and technology developments.

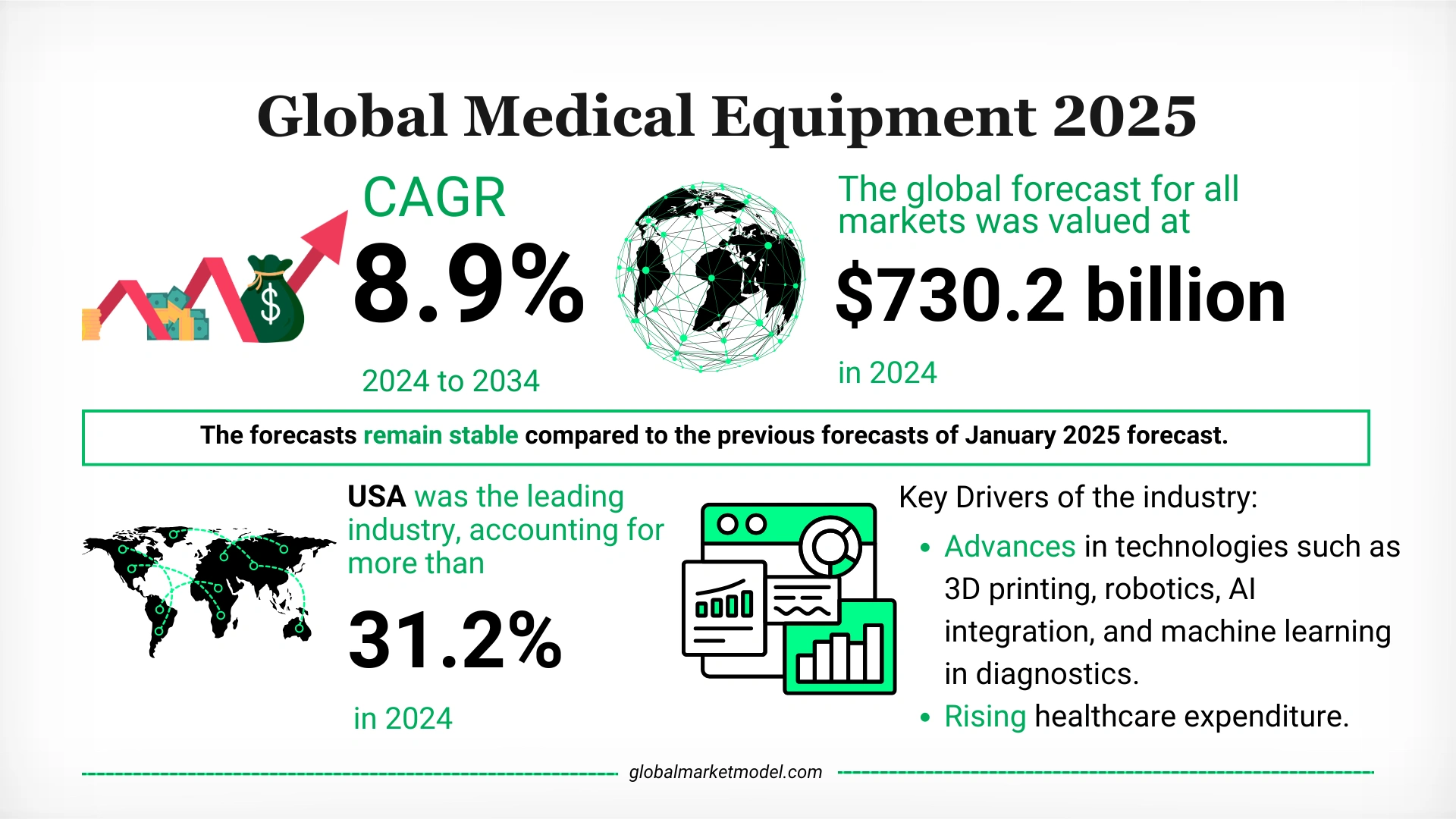

Healthcare Technology Advancements and Preventive Care Priorities to Drive Market Growth: Medical Equipment Industry Overview

Insights from the Global Market Model show how rising healthcare needs, technological integration, and preventive care are shaping the future of the medical equipment industry.

The Global Market Model’s latest forecast highlights the growing scale of the medical equipment market, driven by innovation in diagnostics and increased healthcare expenditure. Here’s a detailed overview of how this vital sector is expected to perform over the next decade.

What Are the Key Market Projections and Insights on Medical Equipment Manufacturing Growth?

Overall Market Growth:

- The global medical equipment market value is at $730.2 billion in 2024.

- The market is projected to grow at a compound annual growth rate (CAGR) of 8.9% from 2024 to 2034.

- In 2024, it represented 0.6% of the global GDP.

Growth drivers include:

- Accelerated adoption of technologies such as 3D printing, robotics, AI, and machine learning in medical diagnostics.

- Increasing healthcare expenditure across both developed and developing nations.

- Rising demand for minimally invasive procedures and a growing shift toward preventive care.

- A large aging population and sustained investment in hospital infrastructure.

What Are the Key Medical Equipment Industry Segments?

Industry Composition:

- The market includes instruments, home medical equipment, apparatus, or machines used in the prevention, diagnosis, and treatment of diseases, as well as in modifying or restoring bodily functions.

- It is supported by a high prevalence of chronic illnesses and strong technological integration in healthcare devices.

Segment Insights:

- The in-vitro diagnostics market was the largest segment in 2024, accounting for 16.7% of the total medical equipment market.

- The United States led globally, comprising 31.2% of the market in 2024.

What Are the Emerging Medical Equipment Industry Trends?

Technology and Home-Based Solutions:

- Growing use of AI-driven diagnostics, home monitoring tools, and minimally invasive technologies continues to enhance patient outcomes and provider efficiency.

- 3D printing and robotics are transforming personalized care and device manufacturing processes.

Healthcare Spending and Preventive Care:

- Rising focus on preventive healthcare is shaping procurement and innovation priorities across regions.

- Healthcare systems are investing in tools that support early detection, remote care, and long-term condition management.

Procurement Delays and Trade Pressures:

- In the last six months, delayed procurement of high-value equipment was observed due to prioritization of essential services and labor-related costs.

- New U.S. tariffs on select imported medical devices have introduced supply chain and pricing uncertainties, especially for products involving cross-border assembly.

How Are Geopolitical and Regional Influences Shaping the Medical Equipment Industry?

United States:

- The U.S. maintains its position as the largest medical equipment market, driven by:

- High healthcare infrastructure investments.

- Strong focus on cutting-edge diagnostic tools.

- Ongoing policy changes around pricing and import regulations.

Global Trade and Policy Impact:

- Tariff adjustments by the United States have increased cost pressures across international markets.

- Global manufacturers are facing uncertainties in sourcing components, especially from trade-dependent regions.

- Despite challenges, diagnostic and monitoring device demand remains strong in both advanced and emerging markets.

What Is the Overall Outlook for the Global Medical Equipment Industry?

The medical devises and equipment industry is set for long-term expansion, fueled by technology integration, rising global healthcare demand, and the transition toward value-based care. While current procurement delays and trade-related challenges introduce short-term constraints, continued demand for advanced diagnostics and home-care solutions provides a stable foundation for sustained market growth.

Gain exclusive insights with the Global Market Model on key medical equipment metrics, including:

- Asthma prevalence rate

- Cancer prevalence rate

- Cerebrovascular prevalence rate

- Dermatitis prevalence rate

- Diabetes prevalence rate

- Glaucoma prevalence rate

- Healthcare - number of employees

- Healthcare - number of enterprises

- Healthcare expenditure

- Hearing loss prevalence rate

- HIV prevalence rate

- Hospital beds

- Hypertension prevalence rate

Want to explore the medical equipment market outlook further? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and sector-specific factors. The current forecast was made in July 2025, revising the previous forecasts made in January 2025.

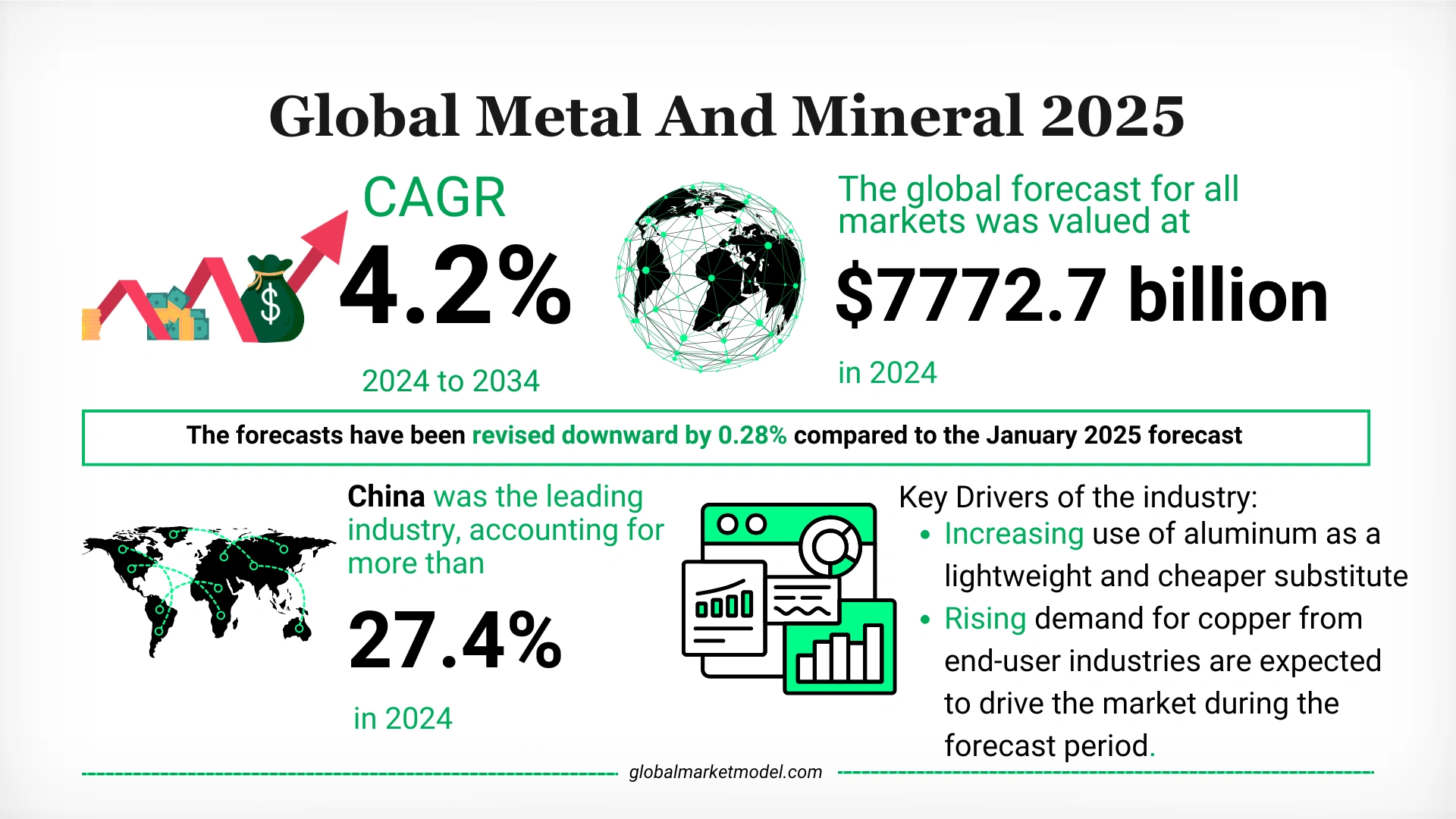

Lightweight Substitution and Energy Transition Demand to Influence Market Growth: Metal and Mineral Industry Outlook

Insights from the Global Market Model highlight how sustainability trends, industrial demand, and policy shifts are shaping the global metal and mineral landscape.

The Global Market Model’s July 2025 forecast offers a comprehensive view of how decarbonization, supply chain pressures, and strategic resource demand are influencing the trajectory of the global metal and mineral market.

What Are the Market Projections and Growth Insights for the Metal and Mineral Industry?

Overall Market Growth:

- The global metal and mineral market is valued at $7772.7 billion in 2024.

- It is projected to grow at a CAGR of 4.2% between 2024 and 2034.

- The sector contributed 6.7% to the global GDP in 2024.

Growth is supported by:

- Increased use of lightweight metals such as aluminum as a cost-effective substitute.

- Growing demand for copper across electrical, construction, and automotive industries.

- Energy transition trends boosting the need for lithium, cobalt, nickel, and rare earths.

- Expanding infrastructure investments and clean energy deployment worldwide.

What Are the Key Segments in the Metal and Mineral Market?

Metal Segment:

- Comprises primary metals such as iron, aluminum, copper, and precious metals.

- Accounts for the largest share (52.9%) of the market in 2024.

- Demand is driven by construction, electricals, manufacturing, and transport sectors.

Mineral Segment:

- Includes industrial minerals and critical resources used in production processes.

- Supports end-uses such as electronics, EV batteries, cement, and steel manufacturing.

Regional Highlights:

- China leads the global metal and mineral market, representing 27.4% of the total in 2024.

- Strong domestic manufacturing, infrastructure projects, and export volumes underpin its dominance.

What Are the Emerging Trends in the Metal and Mineral Industry?

Lightweight Substitution and Electrification Demand:

- Aluminum adoption is rising due to its recyclability, strength-to-weight ratio, and lower cost.

- Electric vehicles and clean energy tech are increasing demand for strategic metals.

Policy and Trade Developments:

- US-imposed tariffs on imported steel, aluminum, and rare earths are creating pricing volatility.

- Trade measures are expected to reshape global sourcing strategies and project budgets.

Industrial Slowdown and Pricing Pressures:

- Sluggish industrial activity and softness in construction and manufacturing are dampening short-term demand.

- Commodity price moderation and delayed projects are contributing to a cautious outlook.

How Are Geopolitical and Regional Influences Impacting Metal and Mineral Market Dynamics?

United States:

- New tariffs are introducing supply chain disruptions and elevating input costs.

- Policy-driven reshoring of key materials may shift sourcing patterns.

Global Trends:

- Weakness in Europe and Asia’s industrial output has weighed on overall consumption in the past six months.

- Despite regional challenges, long-term growth is expected from global industrial recovery and green infrastructure.

What Is the Overall Outlook for the Metal and Mineral Industry?

While the near-term outlook is clouded by industrial sluggishness, trade disruptions, and commodity price pressures, the long-term potential remains strong. Key drivers include electrification, infrastructure development, and increased strategic metal demand. The sector is poised to benefit from global sustainability transitions and industrial expansion initiatives.

Explore in-depth market indicators with The Global Market Model, including:

- Number of enterprises

- Number of employees

Want to know more about the global metal and mineral industry outlook? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually based on economic, geopolitical, and sector-specific trends. The current forecast was made in July 2025, revising the previous version from January 2025.

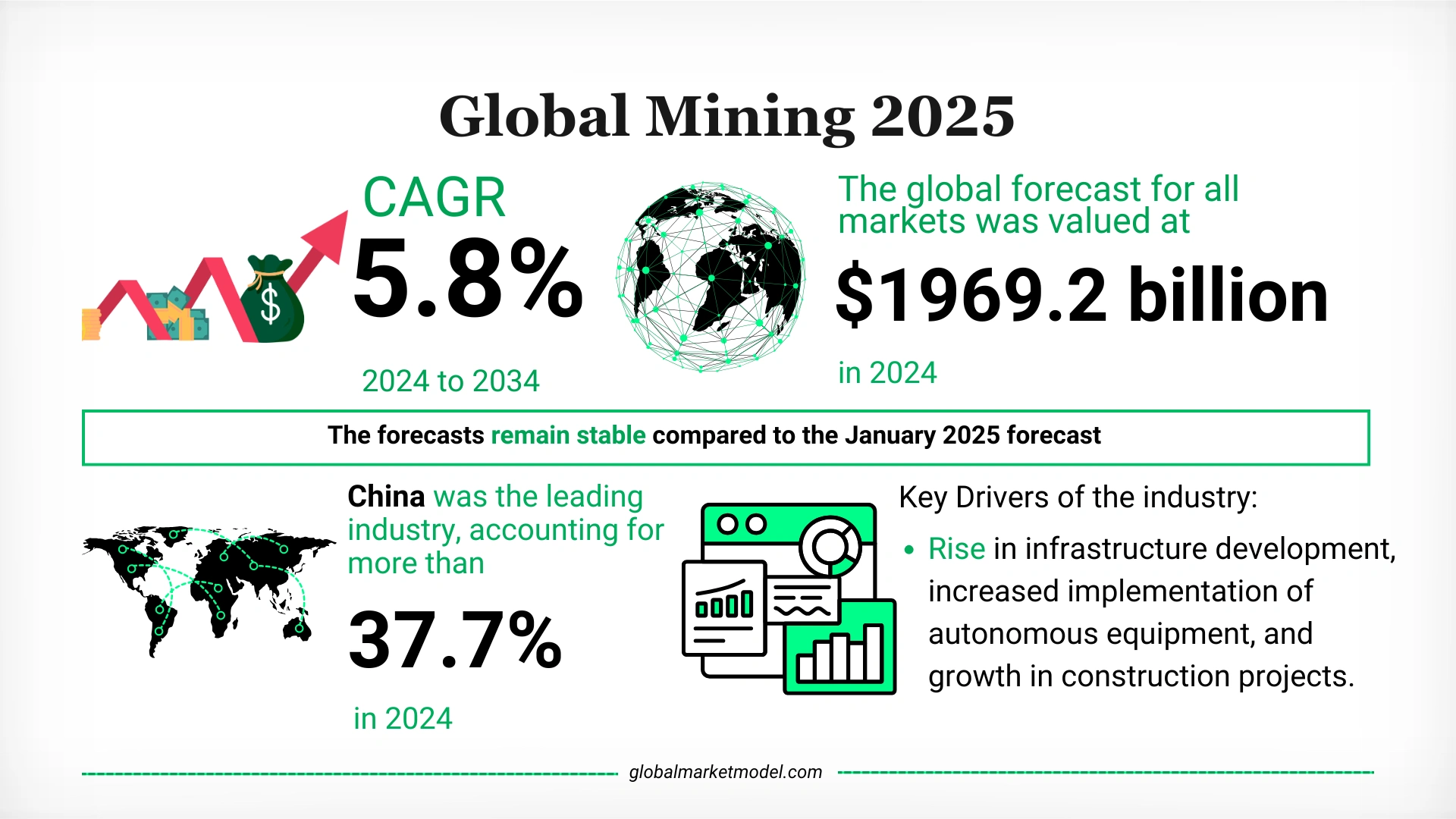

Energy Demands and Green Transitions Reshape the Mining Industry Overview

Evolving infrastructure priorities, rising EV mineral demand, and global resource strategies are steering the future of the mining sector, according to insights from the Global Market Model.

What Are the Market Projections and Growth Insights for the Mining Industry?

- The mining market is projected to grow from $1969.2 billion in 2024 at a CAGR of 5.8% through 2034.

- In 2024, mining contributed 1.7% to the global GDP.

- Growth is supported by:

- Rising infrastructure and construction activity across developed and developing nations.

- Greater use of autonomous equipment in mining operations.

- Increasing demand for minerals used in EV batteries, including lithium, nickel, graphite, and copper.

Which Are the Key Types of Mining Industry?

- Coal mining industry, Lignite, and Anthracite was the largest segment in 2024, accounting for 48.1% of the total market.

- Segment growth is underpinned by:

- Ongoing energy needs and industrial demand.

- Continued dependency on coal in key economies.

- China was the leading market, representing 37.7% of the global mining industry in 2024.

What Are Key Global Mining Industry Trends?

Energy Transition Minerals:

- Demand for minerals crucial to clean technologies has grown due to EV production and renewable energy capacity expansion.

Exploration and Capacity Expansion:

- Companies are investing in new exploration zones and increasing production to meet future demand.

Price and Supply Chain Volatility:

- Although base metal prices have fluctuated, stability is expected as governments implement mineral security frameworks and incentivize local processing.

Policy Shifts and Global Value Chains:

- U.S. trade policy discussions on revising mineral import agreements are prompting shifts in supply chain strategies worldwide.

How Are Geopolitical and Regional Dynamics Influencing the Mining Sector?

- Asia and North America are accelerating renewable energy and EV capacity, strengthening demand for transition minerals.

- Europe and Southeast Asia are launching public-private partnerships and critical mineral strategies to reduce import dependency.

- Trade policies are increasingly geared toward encouraging domestic mineral processing and securing supply chains.

What Is the Overall Mining Industry Outlook?

Despite short-term price fluctuations and logistical challenges, the mining market is positioned for long-term expansion, fueled by sustainable energy goals, infrastructure investments, and increasing demand for critical minerals. The sector’s growth is further supported by technological modernization and proactive government initiatives.

Gain insights on key industry metrics in the mining sector with the Global Market Model, including:

- Number of enterprises

- Number of employees

Want to explore more mining industry trends and forecasts?

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Covering 30,000+ markets, the model is updated twice a year based on economic, geopolitical, and industry-specific developments. The current forecast, published in July 2025, updates the previous edition released in January 2025.

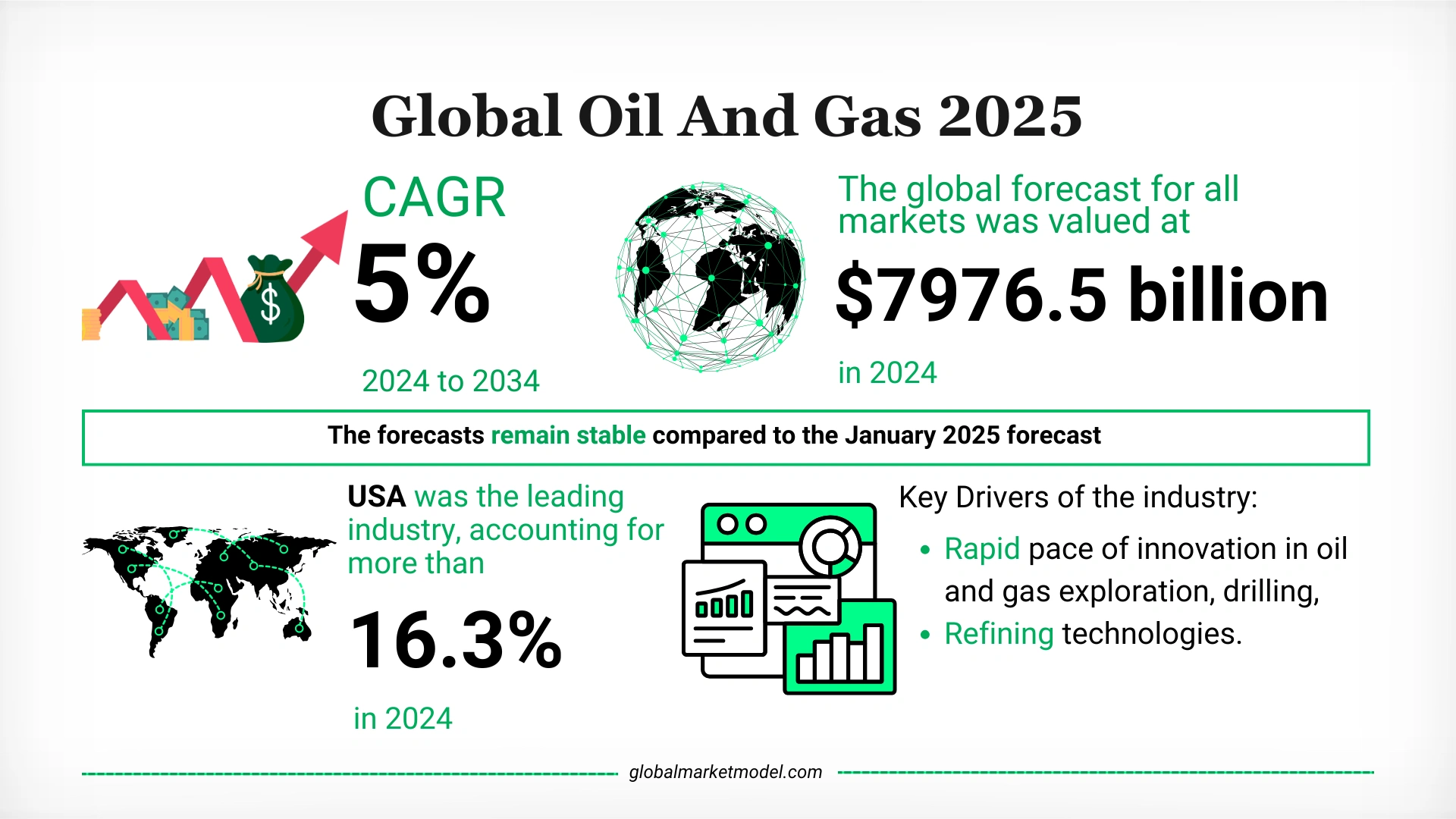

Energy Demand, Supply Dynamics, and Geopolitics Shape Oil and Gas Industry Overview

Insights from the Global Market Model reveal how evolving exploration techniques, production strategies, and geopolitical risks are influencing the oil and gas market long-term growth path.

The Global Market Model’s latest forecast highlights the trajectory of the oil and gas industry, driven by innovation in upstream activities and challenges posed by rising renewables adoption and geopolitical uncertainty. Here's a detailed look at the key forces impacting the sector.

What Are the Key Market Projections and Insights on Oil and Gas Industry Growth?

Overall Market Growth:

- The global oil and gas industry is valued at $7976.5 billion in 2024.

- It is projected to grow at a CAGR of 5% from 2024 to 2034.

- The market accounted for 6.8% of the global GDP in 2024.

Growth is supported by:

- Rapid advancements in exploration, drilling, and refining technologies.

- Enhanced techniques for extracting oil and gas from depleted reserves.

- Development of enhanced oil recovery (EOR) technologies.

- Ongoing exploration activities in untapped regions.

However, increasing cost-effectiveness of renewable energy is gradually expected to impact demand for traditional oil and gas.

What Are the Key Segments in the Oil and Gas Industry?

Upstream Activities Lead the Market:

- The oil & gas upstream activities segment accounted for 57.9% of the total market in 2024.

- Growth is driven by demand for exploration and extraction of petroleum and natural gas from wells.

End-Use Sectors and Market Composition:

- High demand for oil and gas continues from transportation, industrial, residential, and commercial sectors.

- The market plays a central role in the global energy infrastructure.

What Are the Emerging Trends in the Oil and Gas Industry?

Mixed Market Conditions and Trade Challenges:

- Over the past six months, the market has faced mixed conditions, balancing steady demand with trade-related uncertainties.

- Proposed U.S. trade actions on oil-linked products and equipment have raised concerns over supply chain costs and equipment access.

Producer Strategy Adjustments:

- Several producers are slowing expansion plans amid regulatory uncertainty and policy clarity expectations.

- Long-term demand remains tied to economic activity, infrastructure development, and industrial consumption.

How Are Geopolitical and Regional Influences Impacting the Oil and Gas Industry Analysis?

Geopolitical Tensions and Market Stability:

- Conflicts in key production zones such as the Red Sea and Eastern Europe have introduced shipping risks and modest disruptions.

- OPEC+ has continued to manage production strategically to stabilize prices.

United States:

- The USA was the largest market, accounting for 16.3% of the total in 2024.

- Its position is supported by advanced upstream capacity and domestic consumption strength.

What Is the Overall Outlook for the Oil and Gas Industry?

The oil and gas industry continue to be shaped by a dynamic balance of innovation, global demand, and policy factors. While renewable energy gains ground, traditional hydrocarbons remain critical for industrial and residential energy needs. Despite geopolitical tensions and regulatory uncertainty, long-term forecasts remain stable as infrastructure investments and consumption needs support sustained growth.

Gain exclusive insights with The Global Market Model on key industry metrics for the oil and gas sector such as –

- Oil reserves

- Gas reserves

- Active rigs

- Oil refinery throughput

- Oil refinery capacity

- Number of enterprises

- Number of employees

Want to know more about the oil and gas industry outlook? Let us help you!

Request a Demo

The Global Market Model is the world’s largest database of market forecasts. Forecasts for over 30,000+ markets are updated semi-annually on the basis of economic, geopolitical, and industry-specific factors.

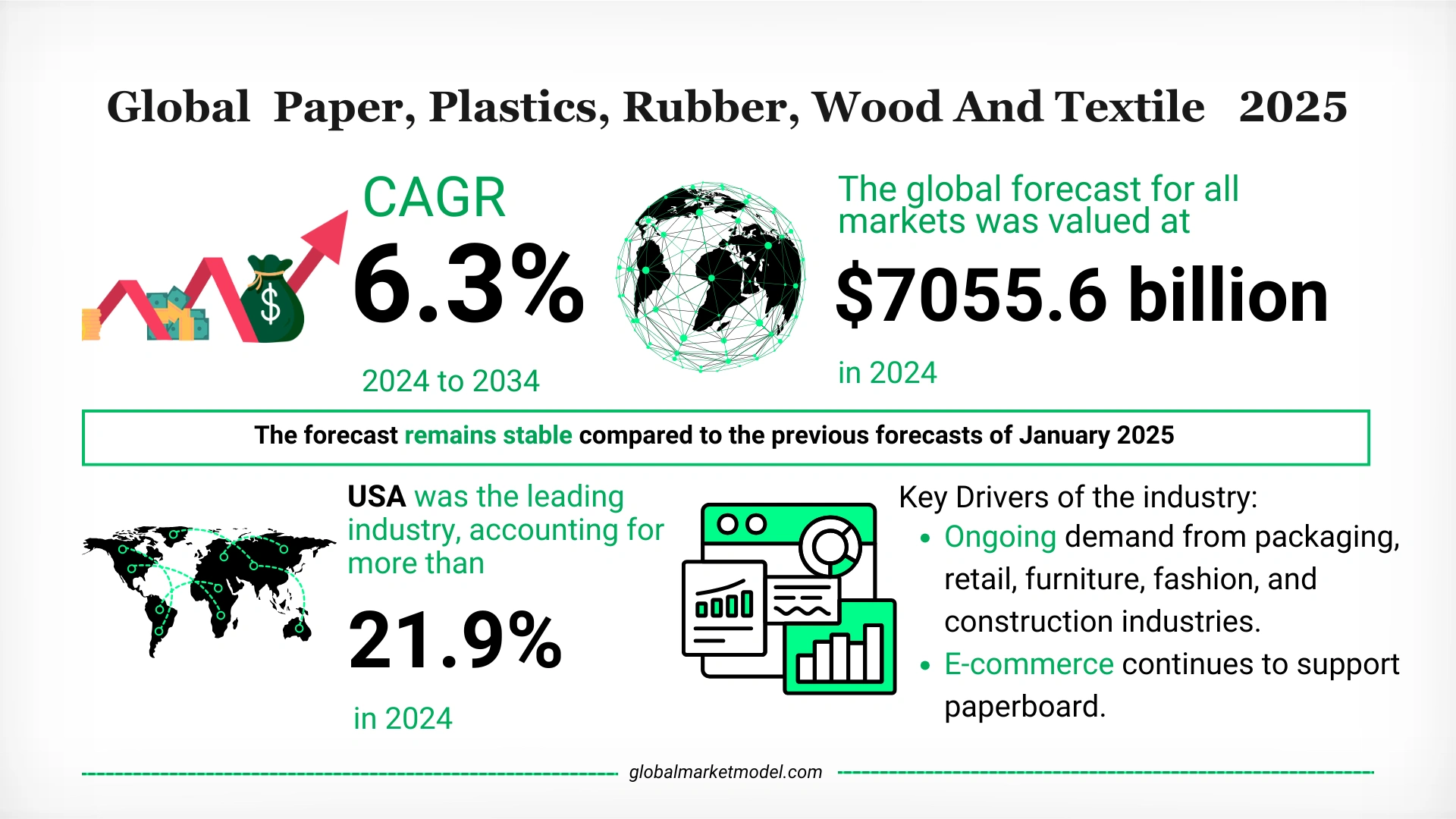

Sustainability Mandates, E-Commerce Demand, and Innovation Reshape Market Outlook: Paper, Plastic Rubber, Wood Industry Overview

Insights from the Global Market Model uncover how environmental regulations, evolving consumer demand, and digital commerce are shaping the future of foundational material industries.

The Global Market Model’s latest forecast highlights a steady upward trajectory for the paper plastic rubber wood industry, fueled by sustainability shifts, growth in e-commerce packaging, and global consumption needs. Here's a comprehensive look at how this diverse market is expected to perform in the coming years.

What Are the Key Market Projections and Insights on Paper, Plastic Rubber, Wood Industry?

Overall Market Growth:

- The global paper, plastic, rubber, wood industry is valued at $7055.6 billion in 2024.

- The market is projected to grow at a CAGR of 6.3% from 2024 to 2034.

- It accounted for 5.9% of global GDP in 2024.

Growth drivers include:

- Expanding demand across packaging, construction, retail, and fashion sectors.

- Increased consumption from e-commerce platforms, especially for paperboard and flexible plastics.

- Regulatory shifts promoting biodegradable and recyclable alternatives.

- Urbanization and rising consumer spending in both developed and developing economies.

What Are the Key Segments in the Paper, Plastic, Rubber, Wood Industry?

Market Composition:

- This industry comprises a diverse range of products derived from pulp, organic polymers, natural fibers, and wood-based materials.

- These materials serve as critical inputs across industries including FMCG, construction, apparel, automotive, and consumer goods.

Plastics and Rubber Products Segment:

- Largest contributor to the overall market, accounting for 20.8% of the total in 2024.

- High demand for durable goods, consumer electronics, and industrial components sustains growth.

Regional Insights:

- USA leads the global market, accounting for 21.9% of total market value in 2024.

- Demand from both industrial production and retail consumption remains strong in North America and Asia-Pacific.

What Are the Emerging Trends in the Paper Plastic Rubber Wood Industry?

Sustainability and Circular Economy:

- Continued shift toward bio-based, compostable, and recycled materials in response to government regulations and consumer preferences.

- Major brands are investing in sustainable packaging solutions and paper recycling systems.

E-Commerce Packaging and Digital Demand:

- Growth in e-commerce is driving demand for innovative packaging, particularly lightweight and protective solutions made of paperboard and flexible plastics.

Discretionary Spending Volatility:

- Recent moderation in consumer demand for apparel, home furnishings, and decorative products has affected production in plastic and wood segments.

How Are Geopolitical and Regional Influences Shaping Market Dynamics?

Trade and Tariff Risks:

- New U.S. tariffs on imports of plastic and rubber products from key manufacturing countries are creating volatility in pricing and sourcing strategies.

- Potential disruptions in global supply chains due to these policies may increase production costs and delay procurement timelines.

Regulatory and Operational Costs:

- Despite stabilization in energy prices, regions face persistently high logistics and compliance costs, impacting manufacturing profitability.

Global Investment Momentum:

- Strong capital inflows into innovation for recycled plastics, biodegradable paper products, and sustainable woods are reinforcing long-term growth prospects.

What Is the Overall Outlook for the Paper, Plastic, Rubber, Wood Industry?

The industry is on a steady growth path, supported by rising consumption, e-commerce expansion, and regulatory shifts favoring sustainable alternatives. While short-term headwinds such as trade policy shifts and raw material fluctuations present operational challenges, the long-term outlook remains optimistic, underpinned by innovation, circular economy initiatives, and industrial diversification.

Gain exclusive insights with The Global Market Model, on the key industry metrics of the paper, plastic, rubber, wood industry market such as –

- Number of enterprises

- Number of employees

Want to know more about this Paper, Plastic, Rubber, Wood Industry?

Request a Demo